T. Rowe Worth manages roughly $1.89 trillion, with about 66% of that cash tied to retirement accounts, advisers, and institutional relationships that the crypto business has spent years making an attempt to achieve.

Its first crypto product, a spot ETP known as TKNZ that started buying and selling on NYSE Arca on July 16, walked straight into the diversified multi-token basket, which is the one nook of the crypto ETF market that has drawn the least cash up to now.

Single-asset spot ETFs monitoring Ethereum, XRP, and Solana have pulled in roughly $13.6 billion mixed, excluding Bitcoin totally. 4 comparable multi-asset merchandise constructed from scratch, NCIQ, EZPZ, TTOP, and TXBC, have gathered about $161 million over the identical tough stretch.

A niche that measurement nonetheless survives the timing caveat.

A forecast that missed the mark

A number of well-known crypto commentators anticipated multi-asset crypto ETFs to be among the many subsequent triggers for institutional adoption.

Matt Hougan argued that many conventional traders haven’t any robust opinion on Ethereum versus Solana and would like broad publicity. Roxanna Islam anticipated the sheer variety of new crypto ETFs to overwhelm adviser due diligence and push consumers towards easier basket merchandise.

Nate Geraci known as himself bullish on one-click crypto publicity, and James Seyffart anticipated index-style crypto ETPs to turn into a serious class this yr.

The shared assumption was that skilled allocators would finally cease choosing particular person tokens and begin shopping for the asset class as a complete.

Pensions and endowments held lower than 5% of spot Bitcoin ETF belongings as of mid-2025, with retail traders nonetheless dominating the class.

A conviction purchaser who needs Ethereum’s restoration or XRP’s funds thesis particularly has little purpose to dilute that wager throughout eight different tokens picked by another person.

Crypto additionally lacks something resembling the S&P 500, a extensively accepted definition of what belongs within the investable market. Each basket has to make its contentious selections about which tokens depend as decentralized sufficient, liquid sufficient, or legally eligible.

Shopping for an index transfers token choice to whoever constructed the index, another person making that very same selection on the client’s behalf.

Hashdex’s NCIQ, one of many cheaper baskets at a 0.25% price, nonetheless sits near 90% Bitcoin and Ethereum, an publicity that the majority traders might replicate with two single-asset ETFs and full management over the weighting.

Diversifying away from Bitcoin throughout a stretch when altcoins have lagged reads as a drag, the alternative of how a bond allocation cushions a inventory portfolio. An adviser explaining a shopper’s stake in a basket of underperforming tokens has a tough dialog.

ProblemWhat traders expectedWhat occurred insteadWhy it mattersBuyer mismatchAdvisers and establishments would like broad crypto exposureRetail and conviction consumers nonetheless dominateToken-specific theses beat summary asset-class exposureWeak diversificationA basket would cut back single-token riskMany baskets stay closely BTC/ETH-weightedInvestors can replicate most publicity with single-asset ETFsNo crypto “S&P 500”Index publicity would really feel neutralToken inclusion remains to be subjective and contentiousBuying a basket outsources token selectionPoor timingAltcoins would make baskets look broader and extra attractiveAltcoins lagged whereas Bitcoin dominatedDiversification seemed like efficiency dragStructural baggageConverted merchandise would validate the categoryLegacy holders exited after ETF conversionsOutflows blurred the sign on new demand

What T. Rowe brings that is new

Bitwise’s BITW has logged roughly $328 million in trailing-year redemptions, and Grayscale’s GDLC noticed heavy withdrawals of its personal as soon as it transformed into ETF type.

Conversion lets legacy shareholders who’d been caught in older, much less liquid buildings lastly exit at web asset worth, so the outflows combine previous holders cashing out with any verdict on new demand.

That conversion baggage nonetheless left the class wanting like a spot traders have been exiting.

TKNZ combines 4 benefits for the primary time on this class. T. Rowe brings the adviser and retirement-platform relationships that the unique basket thesis all the time assumed would present up.

It is also actively managed, free to maneuver weights based mostly on fundamentals and momentum and to carry money or stablecoins when situations flip, an energetic stance instead of the mechanical hold-every-qualifying-token method older baskets used.

T. Rowe can be direct in regards to the fund’s design, brazenly promoting its personal judgment about which tokens deserve the cash.

That mixture turns TKNZ right into a check of three separate explanations for why baskets have struggled: a distribution hole between traders and issuers, a rejection of passive Bitcoin-heavy baskets particularly, or a real choice for selecting tokens immediately.

If TKNZ nonetheless fails to collect actual cash, the third clarification will get a lot more durable to argue in opposition to.

What T. Rowe nonetheless has to show

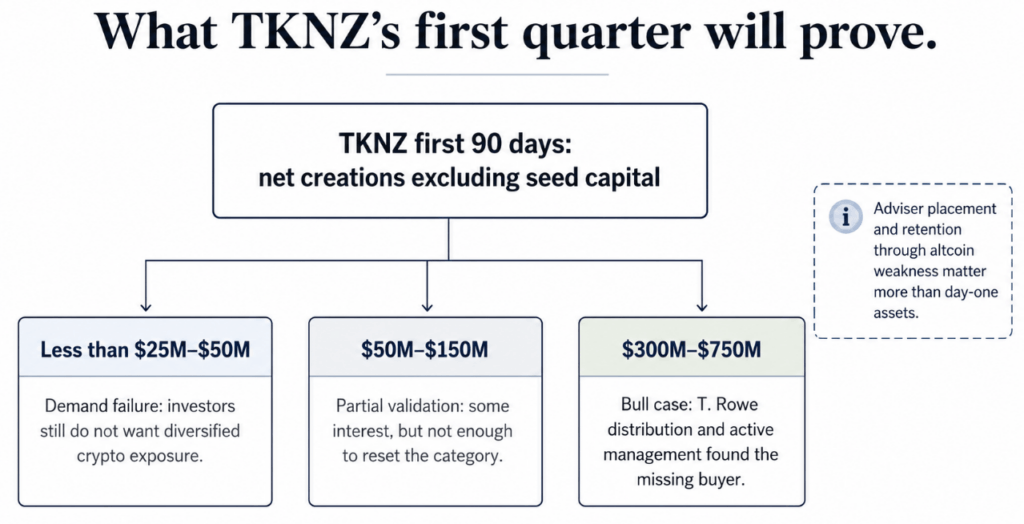

If TKNZ pulls in $300 million to $750 million in web creations over its first quarter, excluding the belongings it launched with, that will present T. Rowe’s distribution and energetic administration can attain cash that the crypto-native basket issuers missed totally.

Actual adviser placement and retention by means of any altcoin weak point would flip this from one fund’s early traction into proof that the basket thesis simply wanted the best issuer.

If web creations keep below roughly $25 million to $50 million with T. Rowe’s title and attain totally deployed, that end result would level out that institutional and adviser demand for diversified crypto publicity should be small at any significant scale.

The proof sits in what TKNZ gathers over its first quarter as soon as seed capital comes out of the depend, whether or not that cash strikes by means of adviser platforms, the channel the unique thesis all the time counted on, and whether or not it stays put by means of the market’s subsequent tough patch for altcoins.

That is the window that lastly tells the business if skilled cash needs crypto as a part of a portfolio.

{kind=link}