Should you use a crypto platform within the European Union or the UK, a few of your 2026 exercise could already be being recorded and will likely be used to feed tax-information studies in 2027.

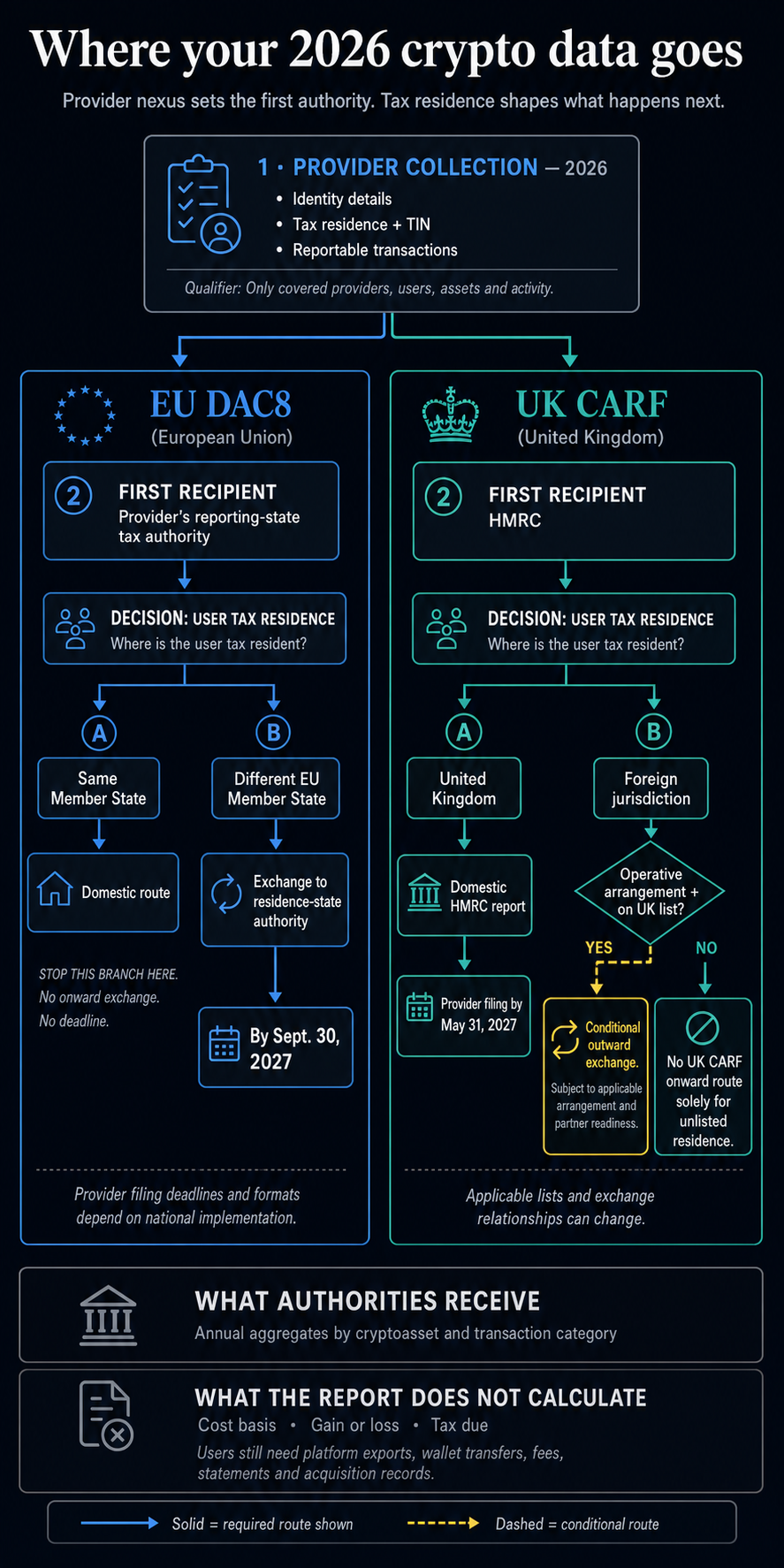

The EU’s DAC8 guidelines and the UK’s Cryptoasset Reporting Framework, often known as CARF, each started making use of on Jan. 1, 2026. The reporting chain now has three distinct phases: a supplier collects info throughout 2026, sends an annual report back to the authority to which it should report, and, in some instances, that authority routes the knowledge to the consumer’s nation of tax residence.

Protection will depend on the supplier, the consumer, the exercise and the related reporting regime.

What suppliers acquire and the place it goes

Beneath DAC8, crypto-asset service suppliers acquire knowledge on reportable transactions involving EU residents, together with customers residing within the supplier’s personal Member State.

UK suppliers acquire figuring out particulars from each consumer, however solely embrace some abroad clients of their annual studies.

HMRC’s assortment steering says lined UK suppliers acquire figuring out particulars for all customers and reportable transaction knowledge for customers within the UK and different CARF international locations. The data could embrace tax residence and tax identification numbers, in addition to reportable transaction knowledge.

The studies acquired by authorities are extra standardized and compressed than the crypto supplier’s underlying data. HMRC describes its submitting as consumer particulars plus a abstract of transactions. DAC8 specifies annual quantitative info, damaged down by reportable cryptoasset and prescribed transaction class.

The supplier’s authorized entity determines the place the account is reported and which authority receives the knowledge first.

For EU suppliers topic to DAC8, the report is first submitted to the authority of their residence nation. UK suppliers ship theirs to HMRC.

The place a consumer lives determines what occurs subsequent. Beneath DAC8, EU international locations share studies on residents utilizing suppliers primarily based elsewhere within the bloc.

UK outward change requires that the international jurisdiction have an settlement or association in impact with the UK and seem on the relevant UK reportable-jurisdiction checklist.

Supplier reporting nexusUser tax residenceFirst recipientWhat can occur nextEU Member State beneath DAC8Same Member StateThat Member State’s tax authorityThe residence and reporting states match, so the knowledge stays within the home route.EU Member State beneath DAC8Different EU Member StateProvider’s reporting-state authorityDAC8 routes the nonresident consumer’s info to the consumer’s residence-state authority.United Kingdom beneath CARFUnited KingdomHMRCThe consumer’s info enters the home HMRC report for the 2026 interval.United Kingdom beneath CARFForeign jurisdiction on the relevant UK listHMRCOutward change can happen when an settlement or association is in impact, and the jurisdiction stays listed.United Kingdom beneath CARFForeign jurisdiction exterior the relevant UK listNone beneath UK CARF solely due to that unlisted residenceIdentity info should still be collected, and a later change to the relevant checklist can alter the international reporting route.

A consumer’s nation doesn’t inform the entire story. What issues is which crypto supplier holds the account, the place that supplier studies, and the tax residence listed for the consumer.

OECD implementation commitments and activated worldwide CARF routes are separate data. The OECD’s exchange-relationships register data path, authorized foundation and relevant dates, and a few relationships may be nonreciprocal.

The 2027 calendar and the boundaries of the report

The UK’s home supplier deadline is fastened. Coated suppliers should submit their first report back to HMRC between Jan. 1 and Could 31, 2027, overlaying exercise from Jan. 1 by way of Dec. 31, 2026, based on HMRC’s reporting steering.

The EU separates when suppliers file studies from when tax authorities change them.

Studies overlaying 2026 are filed in 2027, whereas the relevant Member State units the supplier deadline and format.

Sept. 30, 2027 is the frequent deadline for EU authorities to change info for 2026 about nonresident customers with their EU nation of tax residence. Member State guidelines set every supplier’s submitting cutoff.

UK worldwide change stays conditional after the Could 31 submitting deadline. HMRC’s 2026 reportable-jurisdiction discover requires each an operative settlement or association and inclusion on the UK checklist.

That checklist could change if a jurisdiction defers implementation or the UK concludes one other association. The home submitting date and the conditional outward route are the usable calendar markers; outbound timing follows every relevant relationship.

DAC8’s statutory reporting framework requires annual quantities or honest market values, and models and counts, by reportable cryptoasset and prescribed transaction class. These aggregates present standardized, authority-sanctioned compliance knowledge whereas stopping wanting a whole commerce historical past.

Supplier studies don’t calculate value foundation, features, or tax owed, and so they could miss exercise held on one other change or in a private pockets. When property transfer between a platform and a pockets, the consumer’s data should join each side of the motion and protect the sooner acquisition info that an annual supplier abstract could lack.

This 2026 cycle begins DAC8 and UK CARF reporting, increasing current tax-transparency and tax-compliance channels.

Tax authorities already had different methods to request data or obtain crypto-related info. The present change is the standardized reporting interval now underway throughout these EU and UK regimes.

Information customers ought to reconcile earlier than the studies arrive

Suppliers ship the report, however customers nonetheless want the data to work out what they owe. HMRC’s cryptoasset recordkeeping guide tells people to retain per-transaction info together with the kind, transaction date, purchase or promote standing, models, sterling worth on the time, cumulative models held, financial institution statements and pockets addresses.

Supporting valuation data may additionally be wanted.

Protect the data that allow you to reconnect exercise throughout accounts earlier than an change removes your export or an account is closed.

At a minimal, maintain sufficient info to hint the total historical past of every transaction throughout platforms.

A helpful reconciliation set contains:

full platform exports fairly than screenshots of present balances;transaction dates and timestamps, together with the time zone used;asset names, token identifiers and models;local-currency values at every transaction date;pockets addresses and transaction hashes for transfers;buying and selling, community and withdrawal charges;financial institution, card and change statements;acquisition data and value info from different venues or earlier years; andnotes matching transfers between the consumer’s personal accounts so the identical motion may be traced on each side.

Customers in EU Member States ought to apply the document guidelines and tax strategies of their very own jurisdiction, which can require fields past the UK examples.

The supplier’s 2027 report could present an authority what was declared, but it surely is not going to rebuild the consumer’s full transaction historical past.

Affected customers are already on the reporting clock.

In 2026, customers ought to discover out which supplier holds their account, test the tax residence on file, obtain the total data, and match each transaction towards wallets, statements, charges, and acquisition prices. In any other case, the authority could obtain a abstract that tells solely a part of the story.

{kind=link}