US President Donald Trump signed an government order directing a assessment of laws and obstacles which will restrict fintech innovation and limit entry to banking partnerships and cost programs. The transfer has revived debate round whether or not fintech firms ought to be capable to entry the Federal Reserve’s cost infrastructure extra immediately.

Ought to non-bank fintech companies proceed to depend upon conventional banks to succeed in cost rails, or ought to fintechs entry central financial institution cost rails throughout the US?

TL;DR

US policymakers are reviewing fintech entry to Federal Reserve cost programs after an government order from Donald Trump known as for decreasing obstacles to monetary innovation and updating outdated laws.

On the middle of the controversy is whether or not fintech companies ought to proceed counting on banks for entry to cost rails or be allowed direct entry into core U.S. cost infrastructure.

The dialogue highlights a broader stress between innovation and regulation, as fintech companies push for simpler entry whereas regulators concentrate on stability, oversight, and systemic danger management.

Why Is Entry to Fed Fee Rails So Necessary for Fintechs?

The Fed cost system rails are the core infrastructure that powers how cash strikes throughout the US monetary system. They deal with important monetary actions reminiscent of wire transfers, direct deposits, invoice funds, and real-time settlements between banks and controlled monetary establishments. Due to this position, they sit on the middle of how transactions movement by the financial system.

Proper now, most fintech firms don’t have direct entry to those programs. As an alternative, they function by partnerships with conventional banks that already maintain entry. This implies fintech companies depend upon banking companions to course of funds, maintain buyer funds, and settle transactions throughout the broader monetary system.

This construction creates each operational and strategic constraints. Funds typically transfer by extra layers of processing, which may introduce delays, improve compliance necessities, and restrict how independently fintech firms can construct and scale merchandise. It additionally signifies that a lot of the innovation in digital funds is determined by the infrastructure and permissions of established banks slightly than fintech platforms themselves.

These limitations have additionally formed how competitors works within the funds trade. As a result of banks management direct entry to Fed cost rails, they continue to be central gatekeepers within the system. This makes it more durable for newer monetary firms to compete on equal phrases, even once they provide sooner or extra user-friendly digital companies.

Because of this, entry to Fed cost infrastructure has grow to be a key concern for fintech companies. Higher entry is seen as a option to cut back reliance on middleman banks, simplify cost operations, and develop the flexibility to construct and scale monetary merchandise immediately on high of core cost programs.

On the similar time, the Federal Reserve’s cost programs are thought of important nationwide monetary infrastructure, which is why entry has historically been tightly managed to keep up stability, safety, and reliability throughout the complete monetary ecosystem.

Why the US Authorities Is Reviewing Fintech Entry Guidelines

The talk over entry has intensified as policymakers reassess how monetary innovation needs to be regulated in a digital financial system. The Trump administration has argued that regulatory frameworks must evolve alongside technological change within the monetary sector.

Within the government order, Trump acknowledged that the US stays a world chief in monetary innovation, pushed by the speedy development of economic expertise and fintech companies. Trump wrote:

“To foster this monetary innovation, the Federal Authorities should replace laws to permit integration of digital property and progressive expertise into conventional monetary companies and cost programs. The Federal Authorities should additionally take away overly burdensome and fragmented laws and supervisory practices that kind obstacles to entry and primarily profit incumbent monetary companies companies.”

Regulatory Issues: The Dangers of Fintech Entry To the Fed Fee Infrastructure

Regardless of the rising requires accessibility, the regulators are usually not but prepared to allow non-bank fintechs the appropriate of direct entry into the cost system of the Federal Reserve.

The first concern concerning such an enlargement is the potential to extend systemic dangers. The Fed cost rails deal with a really great amount of high-value transactions every day within the monetary companies trade. Growing the bottom of contributors who’ve direct entry to those rails can result in the potential of failures or different issues, which can have a broader affect throughout the complete monetary system.

The opposite main drawback that wants consideration is oversight. There’s already a well-structured framework out there for overseeing conventional banks. Such guidelines are meant particularly for these organizations that make settlements by themselves. Most fintech firms, together with these that aren’t banks, are regulated in another way, and there are considerations about whether or not these laws can be adequate to grant entry to extra contributors.

One other concern price making an allowance for is that of operational resilience. Fee programs run by the Federal Reserve are anticipated to work faultlessly and with out interruptions. There’s a danger that permitting extra organizations entry may complicate issues and hinder efforts to keep up a correct degree of safety, safety towards fraud, and integrity.

Because of this, entry to the Federal Reserve’s cost system stays extremely restricted. Any steps to open up entry ought to entail establishing extra requirements of compliance and supervision.

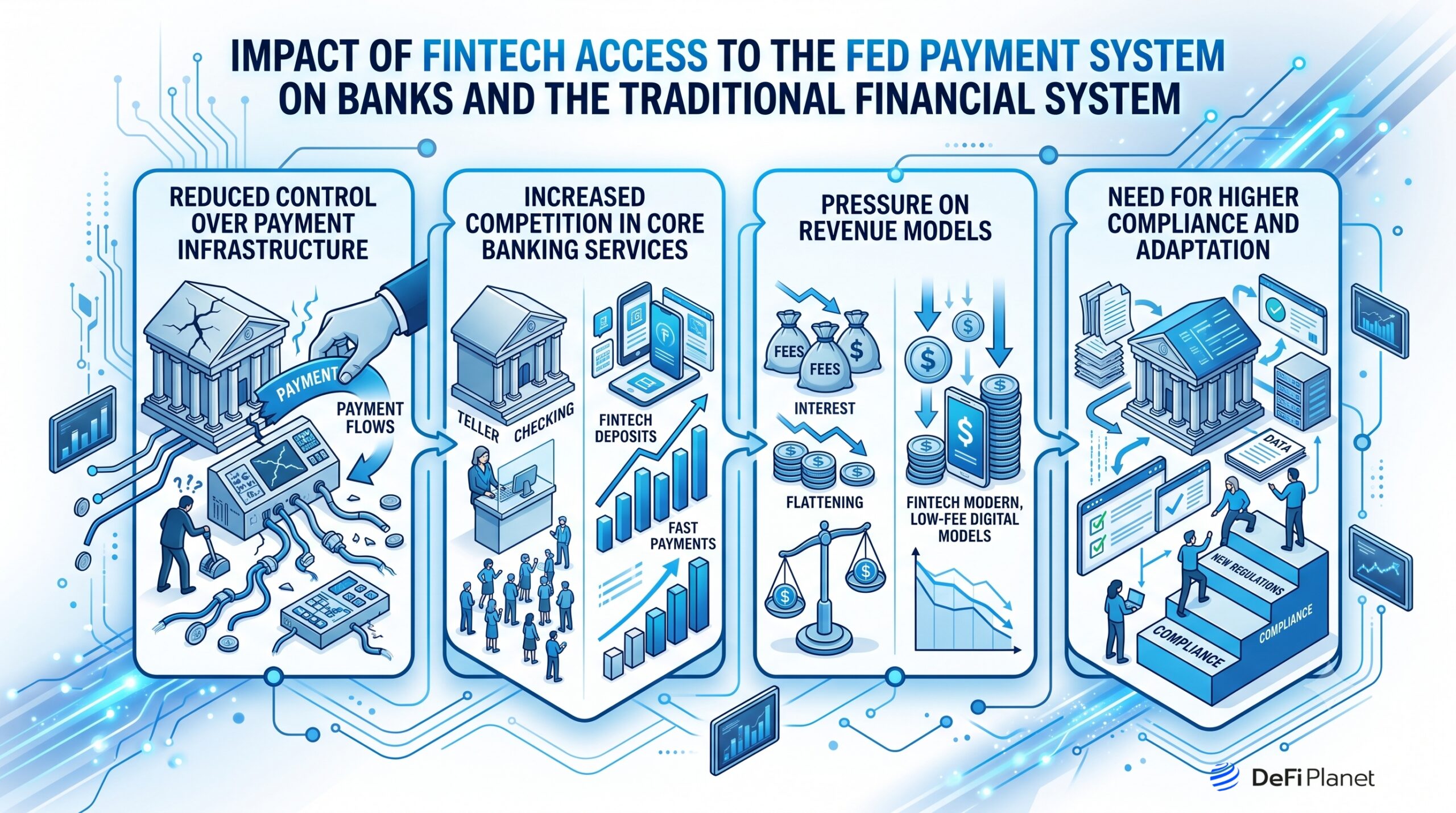

Affect On Banks and the Conventional Monetary System

Increasing fintech entry to the Federal Reserve’s cost programs might reshape how banks function, compete, and keep their position within the monetary ecosystem.

Decreased management over cost infrastructure

Banks at present act as intermediaries for accessing the Federal Reserve’s cost programs. Elevated entry by fintechs can restrict banks’ capacity to keep up management over the infrastructure. It can have an effect on their capacity to regulate one of the vital important facets of the monetary sector.

Elevated competitors in core banking companies

Expanded entry by fintechs can improve competitors in offering companies historically provided solely by banks. These embody transactions and transfers. The strain will likely be associated to cost and repair supply.

Stress on income fashions

The banks obtain a good portion of their income from cost processing and transaction companies. Moreover, many banks derive earnings from appearing as intermediaries in fintech partnerships. Fintechs will discover methods to keep away from intermediaries, resulting in losses in income for the financial institution.

Want for greater compliance and adaptation

The enlargement of entry would require that banks adapt to working with fintechs. That is because of the altering nature of the cost atmosphere.

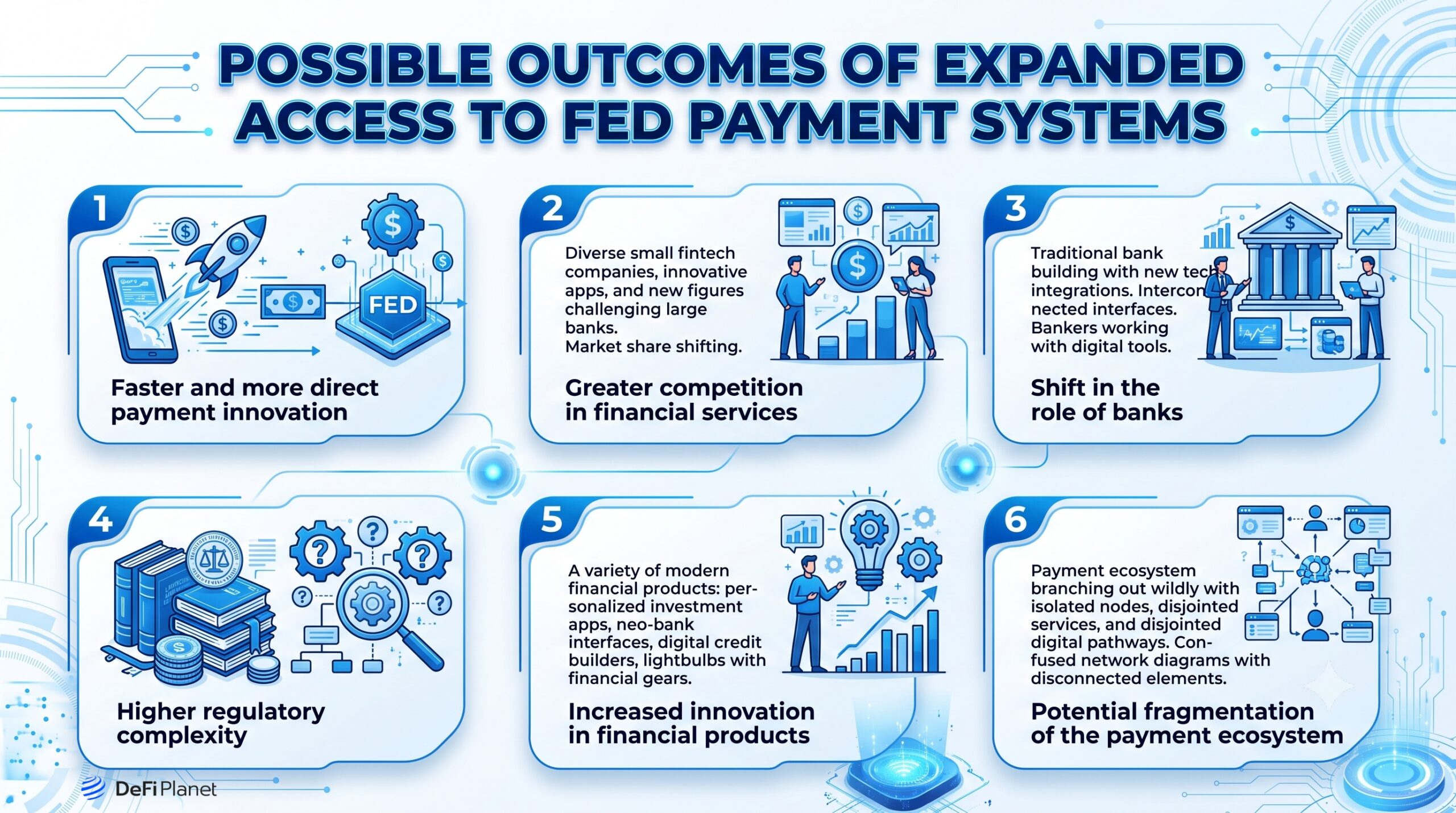

Attainable Outcomes of Expanded Entry to the Fed Fee System

If fintech companies acquire broader entry to Federal Reserve cost infrastructure, it might reshape competitors, innovation, and the construction of the US monetary system.

Sooner and extra direct cost innovation

Fintechs would be capable to develop and introduce their cost options independently of the partnering banks. In flip, this is able to permit accelerating the introduction of improvements reminiscent of real-time funds, automation of varied monetary processes, and embedded finance. Finally, this will speed up the tempo of implementing novel options for purchasers.

Higher competitors in monetary companies

By going on to shoppers and retailers, many Fintechs would be capable to compete within the cost house beforehand unique to established banks. Furthermore, that is prone to result in worth competitors, improved service high quality, and extra shopper decisions for funds and cash transfers. It might additionally diminish the aggressive edge banks maintain in cost ecosystems.

Shift within the position of banks

The position of conventional banks as major suppliers and gatekeepers of cost infrastructure may progressively shift in the direction of compliance, liquidity, and danger administration inside Fintechs. This could imply a diminished position for banks as suppliers of economic companies and an elevated emphasis on supporting infrastructure.

Greater regulatory complexity

The rising variety of entities that immediately hyperlink to the Fed infrastructure would necessitate the event of higher oversight mechanisms to make sure its stability. This might contain nearer scrutiny, enhanced compliance measures, and much more refined instruments to fight fraud and operational danger.

Elevated innovation in monetary merchandise

With wider entry to such a cost system, progressive monetary companies might be created which are at present infeasible throughout the framework of the bank-based monetary sector. Fintech firms may discover the chance to provide you with cost companies which are personalized to clients’ wants.

Potential fragmentation of the cost ecosystem

With the emergence of quite a few contributors immediately linked to the cost system, it’s seemingly that points stemming from the complexity and fragmentation of this atmosphere will come up. Various approaches to coping with completely different facets of the cost course of could complicate its operation.

International Competitiveness Angle (EU, Chinese language Fintech programs)

The talk over fintech entry to the Federal Reserve’s cost programs just isn’t solely a home coverage concern. It additionally has to do with how the US compares with different main economies which are already experimenting with extra open or state-driven cost infrastructures.

Europe’s extra open banking mannequin

Laws such because the Fee Providers Directive 2 (PSD2) within the European Union require banks to share their clients’ account knowledge with any third-party supplier licensed to take action. This observe is called “open banking” and makes it potential for fintechs to create progressive companies constructed on high of typical banking by standardized APIs.

Consequently, funds, knowledge alternate, and monetary companies grow to be rather more interoperable amongst completely different fintech companies. In the US, this instance places strain on the case for introducing a extra versatile entry coverage to speed up fintech improvement.

China’s platform-driven funds ecosystem

A completely distinct instance is China, the place the fintech purposes Alipay and WeChat Pay present cost companies at scale. The platforms work inside an ecosystem that integrates funds, lending, and different monetary companies inside a single ecosystem.

This instance is slightly efficient but additionally demonstrates a extra centralized construction with excessive regulatory scrutiny and the presence of just a few dominant companies.

The US is regulated however fragmented

The US occupies an middleman place between these two programs. On the one hand, it has an especially strong and dependable cost infrastructure. On the similar time, accessibility is decrease because it requires a partnership with banks.

Fintechs could have issue coming into the core cost system by a financial institution, which could take extra time than in additional open nations abroad.

Stress as a consequence of strategic competitiveness

As cost programs proceed to develop, entry to cost infrastructure could grow to be a part of strategic competitiveness in monetary innovation. If US fintech companies face extra restrictions than these in Europe or Asia, the migration of innovation, funding, and expert personnel to different areas could happen.

On the similar time, loosening entry within the US have to be balanced towards the necessity to keep the safety and stability of one of many world’s most important monetary networks.

Are We Headed In the direction of a “Extra Open” Infrastructure System?

The US Fed cost system appears to be like to be shifting towards gradual openness, however most likely not towards a totally open system anytime quickly. Stress from fintech firms and policy-related points could result in higher flexibility and availability over time, particularly for non-bank companies working underneath sure laws.

However the present structure of the cost programs operated by the Fed is not going to bear main adjustments because of the connection between the cost system and monetary stability. The possible situation is a gradual extension and elevated fintech entry, however solely underneath tight regulatory management and never primarily based on an open-architecture method.

Disclaimer: This text is meant solely for informational functions and shouldn’t be thought of buying and selling or funding recommendation. Nothing herein needs to be construed as monetary, authorized, or tax recommendation. Buying and selling or investing in cryptocurrencies carries a substantial danger of economic loss. All the time conduct due diligence.

Loved this? Bookmark DeFi Planet, discover associated matters, and comply with us on Twitter, LinkedIn, Fb, Instagram, Threads, and CoinMarketCap Neighborhood for seamless entry to high-quality trade insights.

Take management of your crypto portfolio with DEFI PLANET PRO, DeFi Planet’s suite of analytics instruments.

{kind=link}