Introduction

Within the early years of cryptocurrency, worth actions have been largely pushed by remoted components: retail adoption, trade hacks, and technological upgrades. Nevertheless, because the asset class has matured and built-in into the broader monetary system, its correlation with conventional macro-economic drivers has tightened considerably. Immediately, Bitcoin operates much less like an remoted digital experiment and extra like a high-beta barometer for world liquidity situations.

To really perceive the cyclical nature of crypto-asset valuations, one should look past the blockchain and analyse the underlying equipment of the fiat financial system. Central to this evaluation is the U.S. Greenback Index (DXY). This text explores the inverse relationship between the energy of the greenback and the efficiency of Bitcoin, positing that the DXY isn’t just a foreign exchange metric, however the major sign for the liquidity tides that raise or sink the crypto market.

The U.S. Greenback Index (DXY) as a Metric of World Tightness

The U.S. Greenback Index (DXY) is technically a measure of the worth of the U.S. greenback relative to a basket of foreign exchange, closely weighted towards the Euro (57.6%), adopted by the Japanese Yen, British Pound, Canadian Greenback, Swedish Krona, and Swiss Franc. Nevertheless, within the context of refined crypto-asset evaluation, viewing the DXY merely as a overseas trade metric is inadequate. It serves a far broader and extra vital perform: it’s the major proxy for world monetary tightness and the shortage of collateral within the offshore banking system.

When the DXY strengthens, rising above key technical ranges akin to 100 or 105, it sometimes alerts a contraction within the availability of {dollars} outdoors america, a phenomenon also known as a greenback scarcity within the Eurodollar market. A stronger greenback is destructive for world liquidity situations as a result of it reduces cross-border credit score development and collateral. As a result of the overwhelming majority of world debt, commerce invoicing, and overseas trade reserves are denominated in USD, a rising DXY will increase the actual debt burden on rising markets, multinational companies, and sovereigns. This forces a liquidation of threat belongings to service dollar-denominated liabilities, making a risk-off atmosphere the place liquidity retreats from the periphery (Bitcoin, Rising Markets Equities) to the core (U.S. Treasuries, Money).

Conversely, a weakening DXY implies an abundance of greenback liquidity. When the greenback falls, monetary situations ease, credit score turns into cheaper to entry, and the “denominator” of world asset costs shrinks. This mechanical devaluation of the measuring stick causes the nominal worth of scarce belongings to rise. That is the basic driver of the Inverse DXY thesis: that Bitcoin rallies are, largely, a repricing occasion pushed by the abundance of the fiat foreign money in opposition to which it’s traded.

Bitcoin because the Final Liquidity Sponge

On this framework, Bitcoin is more and more considered by macro-analysts not merely as a cost know-how or a brand new type of foreign money, however as a direct leveraged play on the debasement of fiat foreign money. Attributable to its mounted provide schedule and its full lack of counterparty threat or money flows, Bitcoin reacts extra violently to adjustments in world cash liquidity (GLI) than conventional equities and even gold.

Raoul Pal, founding father of World Macro Investor, characterizes Bitcoin because the “name possibility on the longer term” and a mechanism that’s coded to rise with world liquidity. The theoretical underpinning right here is that equities, such because the Nasdaq 100, develop on account of a mix of earnings development (GDP) plus financial debasement. Bitcoin, missing earnings, grows on account of community adoption (Metcalfe’s Regulation) multiplied by financial debasement. Consequently, Bitcoin displays a better beta (volatility) relative to the greenback’s actions. When the liquidity channel opens, Bitcoin absorbs this extra capital sooner and extra aggressively than belongings constrained by earnings multiples or bodily provide chains.

Quantitative Evaluation of the Inverse DXY Relationship

The anecdotal principle of a lag is robustly supported by statistical information sourced from market analysts and quantitative researchers. Nevertheless, the correlation isn’t static; it acts as a dynamic variable that strengthens during times of maximum financial intervention and might decouple during times of remoted crypto-market stress (e.g., trade collapses or regulatory bans). To visualise this dynamic precisely, we should first set up a mathematical framework that filters out day by day noise to disclose the underlying structural present.

The Arithmetic Behind the Chart

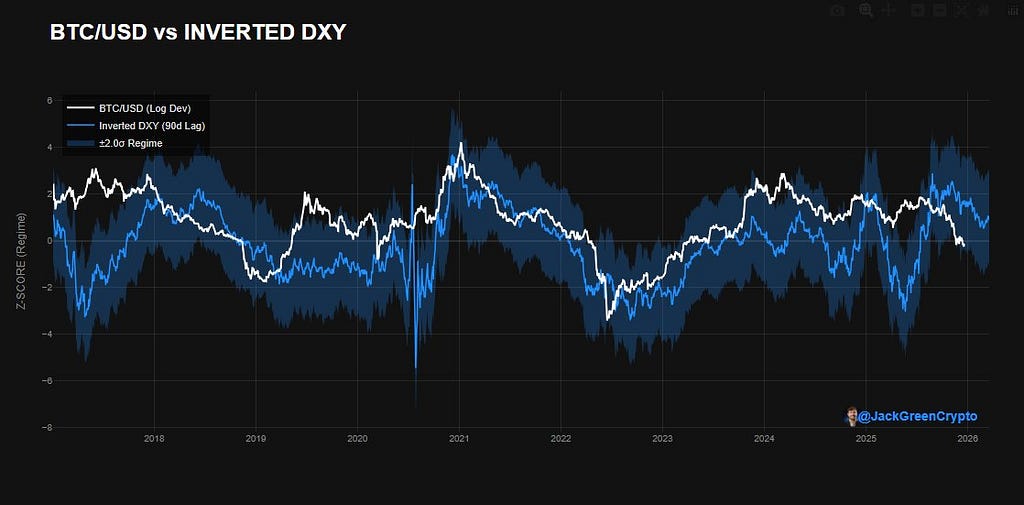

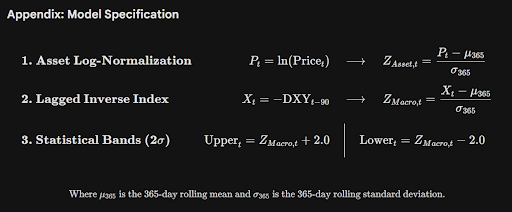

This chart acts as a Macro Regime Filter, visualizing the strain world liquidity exerts on Bitcoin. To make sure statistical validity and comparability between the 2 belongings, the mannequin applies three particular transformations:

Normalization: Bitcoin’s worth undergoes a logarithmic Z-Rating transformation to deal with scale variance and volatility variations. First, a logarithmic transformation is utilized to linearize the asset’s exponential development, making certain that share adjustments are weighted equally throughout distinct market cycles somewhat than being skewed by absolute worth ranges. Second, the information is standardized in opposition to a 365-day rolling window. This normalizes Bitcoin’s excessive inherent volatility relative to the Greenback, changing uncooked worth motion into items of statistical deviation. This enables for a direct, magnitude-agnostic comparability of momentum relative to the asset’s personal yearly pattern.Forecasting (The Unbiased Variable): The US Greenback Index (DXY) is inverted and shifted ahead by 90 days. This lag introduces a predictive forecast window, projecting how previous contractions or expansions in world liquidity are more likely to impression threat asset valuations within the current.Regime Definition (The Clouds): A 2-standard deviation band is utilized to the Driver. This defines a statistical confidence interval. When Bitcoin trades inside these bands, its worth motion is in line with the prevailing macro atmosphere. Deviations outdoors these bands sign statistically important decoupling occasions, the place remoted crypto-native drivers override world macro currents.

Historic Correlation Information: The Jamie Coutts Mannequin

With the mathematical framework established, we will look at the historic efficiency. Evaluation of market information supplied by Jamie Coutts (@Jamie1Coutts) of Actual Imaginative and prescient and Bloomberg Intelligence (March 2025) highlights the predictive energy of DXY actions on Bitcoin’s worth. Coutts’ analysis focuses on the magnitude of DXY declines and their subsequent impression on BTC returns over a 90-day window. This impulse primarily based evaluation filters out day by day noise to give attention to structural shifts.

Desk: Bitcoin Efficiency Following Vital DXY Declines

Supply Information:

The information signifies a remarkably excessive diploma of statistical significance. A speedy depreciation of the greenback (>2.5% in 3 days) has traditionally served as an ideal “purchase sign” for Bitcoin, however the returns are realized over the following three months, confirming the lag thesis. The “win charge” of 94–100% for important DXY drops signifies that the inverse relationship is among the most dependable alerts within the crypto-asset market.

Volatility-Adjusted Correlation

An vital nuance within the quantitative evaluation is the altering volatility profile of Bitcoin. Constancy Digital Property reported that by late 2023 and into 2025, Bitcoin’s volatility had declined beneath that of many S&P 500 constituents.

As Bitcoin’s volatility compresses, its sensitivity to DXY actions could change. A lower-volatility asset requires bigger liquidity injections to maneuver the needle, or conversely, it could monitor the inverse DXY extra carefully (linear correlation) somewhat than performing as a leveraged guess (exponential correlation).

Conclusion

Because the digital asset class matures, the digital gold narrative is evolving right into a extra nuanced actuality: Bitcoin is a hyper-sensitive gauge of world greenback liquidity. The inverse relationship with the DXY supplies a sturdy, although dynamic, framework for understanding worth cycles. Whereas onchain metrics and technological updates stay related, one in all Bitcoin’s primary worth drivers within the medium time period will probably be the shortage or abundance of the US Greenback.

Need Extra? Comply with the Writer on X

Bitcoin’s Hidden Driver: The Inverse DXY Relationship was initially printed in The Capital on Medium, the place persons are persevering with the dialog by highlighting and responding to this story.

{kind=link}