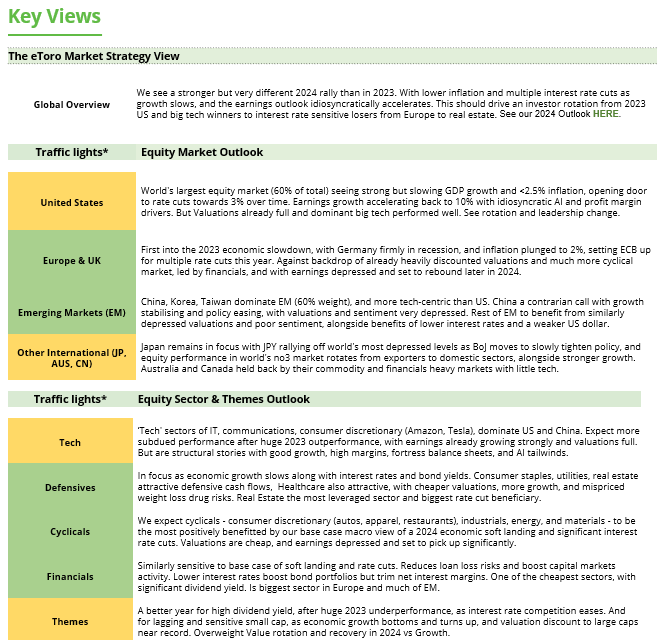

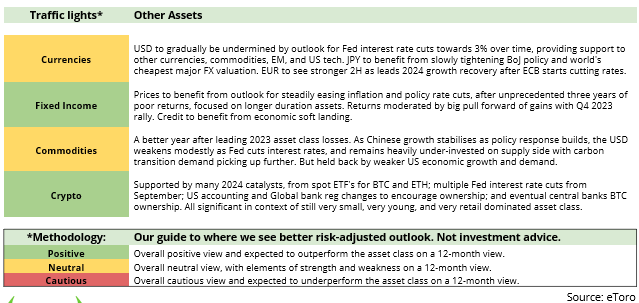

Please see this week’s market overview from eToro’s world analyst group, which incorporates the newest market knowledge and the home funding view.

Markets cheer on Trump’s return to the workplace

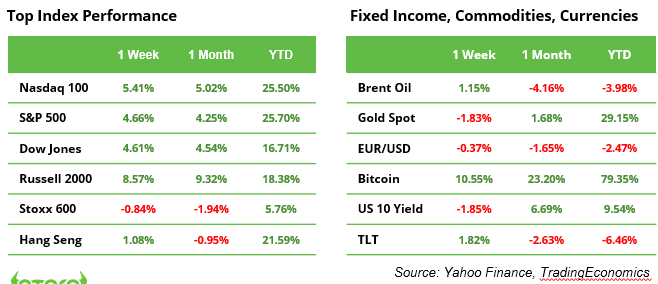

Along with his return to the White Home, Donald Trump has change into solely the second American “boomerang” President after Grover Cleveland in 1893. Fairness markets cheered, very similar to in 2016, on the promise of decrease taxes and diminished regulation. On 6 November, the S&P 500 rose by 2.5%, the Nasdaq gained 3.0%, and the Dow Jones elevated by 3.6%, setting new information led by the anticipated “Trump sectors” (see desk). The small-cap Russell 2000 surged by a powerful 5.8%, pushed by expectations of a extra beneficial local weather for deal-making and company takeovers.

Bond “vigilantes,” fearing larger debt and elevated inflation underneath Trump’s management, pushed the US 10-year yield as much as 4.5%. Bitcoin soared by 9% on Wednesday and maintained its momentum to achieve the $80,000 stage for the primary time ever over the weekend. The US greenback strengthened to 1.07 in opposition to the euro, marking one of the best week for the buck since 2020. Tesla inventory jumped by 29% in every week, as traders consider Elon Musk will likely be rewarded handsomely for his robust assist throughout the election marketing campaign.

In “different information”, the Fed minimize its coverage rate of interest by 0.25%, bringing it to a variety of 4.50% to 4.75%. In the meantime, Germany noticed its coalition authorities collapse (see subsequent web page), and China unveiled a $1.4 trillion stimulus package deal that underwhelmed traders. The US has ordered Taiwanese chipmaker TSMC to halt shipments of essentially the most superior chips to China. The commerce warfare between these two world powers is intensifying by the day, at the same time as Trump’s second presidency has but to start.

The week forward

Within the US, traders will obtain October CPI numbers on Wednesday, and October retail gross sales on Friday. Moreover, the Q3 earnings season will proceed with, amongst others, outcomes from House Depot, Cisco, Disney, and Utilized Supplies, German High 5 shares Siemens, Deutsche Telekom and Allianz, and China’s retail giants Alibaba, Tencent and JD.com.

Desk. S&P 500 Index sector efficiency after Trump’s victory was introduced

Supply: Google Finance. Worth returns in USD between 5 and eight November 2024

Are renewable power shares bought off unjustified?

Following Trump’s “drill, child, drill” election, renewable power shares took a major hit. Enphase Power dropped 26%, Vestas Wind, regardless of reporting earnings, fell 23%, and Plug Energy decreased by 18%. The sector faces robust headwinds from decrease fossil gas costs and better tariffs on elements imported from China, which threaten to decelerate the expansion of photo voltaic, wind, and hydrogen applied sciences. Nevertheless, the rising power calls for of chip manufacturing and AI knowledge facilities could hold all obtainable power sources in demand. The sell-off appears to be extra of a market overreaction to fast political modifications fairly than a mirrored image of the sector’s future potential.

Authorities disaster in Germany, Scholz plans new elections by March

The “site visitors mild coalition” of the SPD, Greens, and FDP has collapsed. Chancellor Olaf Scholz has fired Finance Minister Christian Lindner after clashes over the 2025 price range. Scholz needed elevated investments to revive the stagnant economic system, however Lindner refused to breach the debt brake, citing his oath of workplace.

With solely a weakened SPD-Greens minority authorities, reforms at the moment are troublesome. This uncertainty exacerbates Germany’s fragile economic system, particularly the struggling automotive sector. The Commerzbank takeover by Italy’s UniCredit provides to the chaos, delaying vital infrastructure and renewable power tasks.

The disaster is pushing Germany towards new elections. The opposition calls for a vote of confidence this week, however Scholz plans to delay it till mid-January to finalize tasks. Elections might occur by late March, following the 60-day constitutional timeline.

Earnings and occasions

Interesting corporations on three continents will report earnings this week. As well as, semiconductor gear maker ASML will host an Investor Day, updating its 2030 outlook.

Earnings releases:

12 Nov. House Depot, Shopify, Spotify, Softbank, Occidental Petroleum

13 Nov. Cisco, Tencent, Allianz

14 Nov. Disney, Utilized Supplies, JD.com, Siemens, Deutsche Publish + ASML Investor Day

15 Nov. Alibaba

This communication is for info and training functions solely and shouldn’t be taken as funding recommendation, a private suggestion, or a suggestion of, or solicitation to purchase or promote, any monetary devices. This materials has been ready with out making an allowance for any explicit recipient’s funding targets or monetary scenario and has not been ready in accordance with the authorized and regulatory necessities to advertise impartial analysis. Any references to previous or future efficiency of a monetary instrument, index or a packaged funding product usually are not, and shouldn’t be taken as, a dependable indicator of future outcomes. eToro makes no illustration and assumes no legal responsibility as to the accuracy or completeness of the content material of this publication.

{kind=link}