SOFI inventory has been hammered from its highs, but its development estimates stay promising. The Each day Breakdown digs into the dip.

Thinking about extra Deep Dive content material? Take a look at our newest analysis.

Deep Dive

It’s been a risky run for SoFi Applied sciences, with shares down virtually 40% to date this yr. Even so, the inventory remains to be up about 50% over the previous yr and even traded beneath $5 as just lately as Could 2023. So what’s the story behind this roughly $20 billion financial institution?

SoFi Applied sciences is a digital monetary providers firm that provides banking, lending, investing, and different money-management merchandise by way of a single app. It positions itself as a one-stop platform aimed toward serving to members borrow, save, spend, make investments, and defend their cash.

When SoFi started buying and selling publicly in 2020, the inventory opened round $11 earlier than shortly climbing into a large buying and selling vary of roughly $14 to $24. The following bear market then dragged shares into the one digits, with the inventory falling as little as $4.24. Regardless of that volatility, the enterprise has continued to develop. As proven above, SoFi’s three largest companies have expanded annually, whereas complete adjusted gross revenue has additionally continued to climb.

Future Progress Projections

So far as analysts are involved, that development ought to proceed into the long run, too. In line with Bloomberg, analysts mission the next:

Earnings Progress: 56% in 2026, 32% in 2027, and 23.5% in 2028

Income Progress: 30.1% in 2026, 21.3% in 2027, and 13.9% in 2028

Analysts at the moment have a consensus worth goal of ~$23.88 on SOFI inventory, implying about 47% upside to immediately’s inventory worth.

Wish to obtain these insights straight to your inbox?

Enroll right here

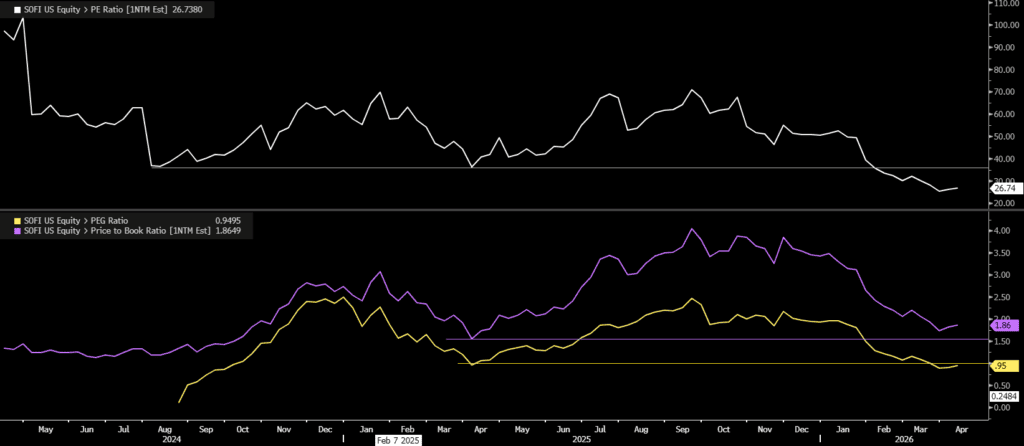

Diving Deeper — Valuation

Valuing youthful corporations with robust development could be troublesome. In SoFi’s case, although, that development has helped make the valuation extra cheap:

The ahead P/E ratio is now close to a multi-year low of roughly 26.5x, whereas the price-to-book ratio — a typical measure for financial institution shares — is beneath 2x and close to the 2025 low, (despite the fact that the inventory worth is up about 90% from that interval).

Lastly, SoFi’s PEG ratio — which measures valuation relative to anticipated earnings development — is again beneath 1.0. A standard rule of thumb is {that a} PEG ratio round 1.0 suggests a inventory is pretty valued, beneath 1.0 could point out undervaluation, and above 1.0 can indicate the inventory is pricey relative to its development.

Dangers

A few of SoFi’s foremost company-specific dangers embrace its heavy publicity to private lending and credit score efficiency, reliance on deposits and capital-markets funding to help mortgage development, and regulatory and compliance threat tied to working a nationwide financial institution. Elements of the enterprise, notably pupil lending, are additionally delicate to rates of interest and authorities coverage. Like all banks and lenders, SoFi would additionally face broader recession threat, together with weaker mortgage demand and better credit score losses.

The Backside Line

The bull case is that SoFi remains to be rising, its ecosystem is maturing, and after such a steep drop from the highs, the valuation is much simpler to abdomen. The bear case is that that is nonetheless a shopper lender and financial institution dealing with credit score, recession, funding, and regulatory dangers. So whereas the selloff has helped de-risk the inventory, traders nonetheless want confidence that development can outweigh these headwinds.

Disclaimer:

Please be aware that as a consequence of market volatility, a number of the costs could have already been reached and eventualities performed out.

{kind=link}