Analyst Weekly, January 26, 2026

This week brings a flood of high-impact earnings from megacaps and sector bellwethers throughout tech, semiconductors, healthcare, shopper, industrials, and power. Markets are wanting past headline beats or misses: the main target is squarely on pricing energy, demand resilience, value self-discipline, and the way administration groups are framing 2026. Under are the important thing earnings to look at and what’s more likely to transfer every inventory.

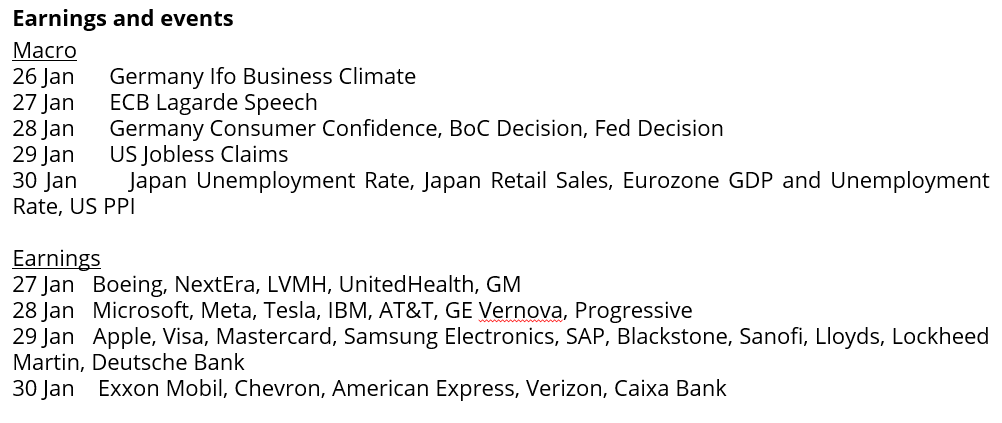

Microsoft (MSFT). Focus: The inventory’s response will hinge on Azure cloud development and AI providers.Traders are targeted on cloud demand and margins: Microsoft’s AI-driven income backlog (together with main OpenAI and Anthropic commitments) is big, so any replace on cloud development charges, AI monetization, or steerage might be key. Market Response Drivers: Sturdy Azure and AI outcomes (or a steerage shock) might reinforce the view that Microsoft’s hefty AI investments are paying off, whereas any signal of cloud deceleration would possibly elevate valuation worries.

Meta Platforms (META). Focus: Meta’s earnings are extremely anticipated as a gauge of digital advert well being. The important thing inventory driver might be whether or not Meta can maintain robust promoting development and present expense self-discipline. Traders’ focus areas embody advert traits, the outlook for 2026 bills, and the continuing Actuality Labs losses. Market Response Drivers: Meta has began reining in its metaverse ambitions after Actuality Labs’ cumulative losses topped $70B. Any updates on value cuts there, alongside commentary on person engagement or new monetization (like adverts on Threads), will closely affect sentiment.

Apple (AAPL). Focus: On the earnings name, traders will pay attention for updates on its AI partnership and steerage on margins, in addition to any hints about new merchandise (AR/VR units or a foldable iPhone) and the way Apple plans to navigate commerce headwinds in 2026. Market Response Drivers: iPhone gross sales and providers development are anticipated to drive double-digit income and EPS good points, however the primary catalyst could also be Apple’s rising AI technique. In truth, Apple simply struck a multi-year deal to make use of Google’s Gemini AI fashions to energy Siri and future merchandise: a transfer analysts say lastly addresses the “invisible AI” hole in Cupertino’s technique.

Tesla (TSLA). Focus: The largest driver of Tesla’s inventory response might be automotive revenue margins, which have been squeezed to multi-year lows by value wars. Traders are hoping to see indicators that gross margins have stabilized or that Tesla’s power storage enterprise (which now enjoys larger margins than autos) can offset weak point. Market Response Drivers: Tesla’s commentary on order backlogs in China/Europe, the uptake of its FSD (self-driving) subscriptions, and progress on the robotaxi fleet or Optimus humanoid robotic might be intently scrutinized. Any constructive surprises, better-than-expected margins or concrete timelines for these tasks, might swing the risky inventory.

Boeing (BA). Focus: Boeing reviews after a robust run: the inventory jumped ~23% in 2025 on hopes of an aviation upcycle. The corporate lastly returned to constructive earnings and expects a ~46% YoY income soar in This autumn as deliveries hit their highest since 2018. Market Response Drivers: Traders are on the lookout for Boeing to verify larger jet manufacturing charges and bettering money technology. Free money move steerage for 2026 might be vital as properly: if the corporate indicators money flows will considerably rise subsequent yr, it will validate the bullish case. Conversely, any hiccups in hitting these manufacturing targets or cautious commentary on supply-chain dangers might mood the passion round Boeing’s restoration.

ASML Holding (ASML). Focus: ASML reviews on 28 January, and the main target is not going to solely be on income, but in addition on orders. Sturdy demand from TSMC and reminiscence makers like Samsung might sign a robust setup for development into 2027, even when 2026 seems to be constrained. Market Response Drivers: Traders will watch whether or not This autumn orders land round €7bn and the way administration frames 2026 steerage. Commentary on the trajectory of China-related gross sales, now anticipated to say no beneath export controls, can even matter. If ASML indicators that different areas are ramping quick sufficient to offset this, it might ease geopolitical overhangs. Even when near-term income development seems to be modest, robust orders would reinforce confidence that ASML’s AI- and memory-driven cycle nonetheless has loads of runway.

Visa (V) & Mastercard (MA). Focus: Visa and Mastercard report on 28 January, with the concentrate on shopper spending traits, cross-border volumes and administration commentary fairly than headline earnings beats. Secure card utilization and resilient journey demand would help confidence in continued low-double-digit income development, regardless of elevated regulatory noise. Market Response Drivers: For Visa, traders will watch spend indicators and commentary on incentives and pricing, whereas Mastercard’s preliminary framing of 2026 steerage and providers momentum might be key. Even largely in-line outcomes might assist stabilise sentiment if each corporations reassure markets that volumes stay wholesome and regulatory dangers are manageable.

Exxon Mobil (XOM). Focus. In 2025, oil costs fell virtually 20%; Brent averaged within the low $60s which can drag on Exxon’s This autumn earnings. Exxon has already warned that decrease crude costs probably reduce its upstream revenue by as much as $1.2 billion versus Q3, although stronger refining margins might offset a number of hundred million. Market Response Drivers: Traders will search for confidence that quantity development and value cuts can drive sturdy money move even at decrease oil costs. Key focus areas embody Exxon’s 2026 capital spending plans, any updates to its lately raised 2030 revenue outlook (Exxon boosted its long-term earnings/money move targets with out larger capex), and the way it will deploy its “surplus” money (dividends, buybacks). If Exxon underscores its resilience and guides to stable money technology at $60 to $70 oil, it might uplift the entire power sector.

Gold Is Changing Bonds because the Most popular Hedge

Gold is more and more being utilized by traders as a hedge towards fairness danger, displacing long-duration Treasuries. The shift displays a structural breakdown within the conventional equity-bond relationship: since 2022, correlations have hovered close to zero, eroding bonds’ effectiveness as a diversifier.

Traditionally, length publicity cushioned drawdowns in danger belongings. However current episodes, just like the post-Liberation Day drawdown the place equities and lengthy bonds offered off in tandem, have undermined confidence in bonds as a dependable hedge.

Funding Takeaway: Gold has held up as a defensive asset. Flows present traders allocating to equities and gold concurrently, whereas lowering publicity to longer-dated bonds. The pattern displays greater than inflation hedging and a reallocation of portfolio danger administration. If the bond-equity correlation stays unstable, the position of gold as a volatility dampener might grow to be extra entrenched, redefining how portfolios hedge draw back danger over the cycle.

Netflix Inventory After a Turbulent Week: Promote-Off Halted – What’s Subsequent?

Netflix shares skilled a extremely risky week. Promoting stress initially accelerated. Whereas the quarterly outcomes had been stable, the outlook was perceived as extra cautious. At its low, the inventory fell by practically 9% to $80.26.

Later within the week, a rebound set in, limiting the weekly loss to round 2%. Netflix ended the week at $86.12. The temporary drop additionally resulted in a false breakdown under the January and April 2025 lows.

On the similar time, an vital help zone (honest worth hole) between $79.72 and $80.81 was efficiently defended. Truthful worth gaps characterize market inefficiencies. The lengthy decrease wick on the weekly candle, mixed with the protection of this zone, factors to a possible stabilization.

Within the coming weeks, traders ought to look ahead to additional affirmation indicators, resembling a sequence of upper highs and better lows, which might point out the formation of a brand new uptrend. The inventory is at the moment buying and selling about 36% under its all-time excessive.

Netflix, weekly chart. Supply: eToro

Meta Inventory at Resistance: Earnings because the Key Catalyst

Meta shares gained 6.4% final week, closing at $658.76. This transfer has pushed the inventory into a well known resistance zone (honest worth hole) between $658.13 and $715.30. An space the place consumers have been rejected a number of occasions since early December.

The important thing short-term catalyst is earnings on Wednesday night. A sustained transfer above the 20-week shifting common at $663.85 could be a primary constructive sign. A breakout above the intermediate excessive at $685.75 would additional enhance the technical image.

In that situation, the chance will increase that the inventory might retest its all-time excessive at $795. For context, Meta had declined by round 27% between August and November, and that hole has now been diminished to roughly 17%.

On the draw back, a robust help zone (honest worth hole) between $548.90 and $588.72 has up to now prevented deeper pullbacks. Ought to a short-term retracement happen, this space might as soon as once more act as a help zone.

Meta, weekly chart. Supply: eToro

Meta, weekly chart. Supply: eToro

Rising Markets: Fifth Weekly Acquire in a Row – How Sustainable Is the Rally?

The iShares Core MSCI Rising Markets ETF rose by 2.3% final week, reaching a brand new file excessive and marking its fifth consecutive week of good points. Not too long ago, a rotation of capital away from US belongings towards Asia and rising markets has been noticed. The upward momentum that started in mid-December is now properly superior.

Nevertheless, the speedy value enhance has created new honest worth gaps at $68.90–$70.04 and $67.28–$69.01. Truthful worth gaps characterize market inefficiencies and are sometimes revisited by value at a later stage (see the earlier instance highlighted in orange on the chart from September to December).

These areas can due to this fact function potential areas of curiosity for consumers. What issues most, nonetheless, is the market’s response. The zone mustn’t solely be reached but in addition revered. Solely with affirmation, resembling stabilization or clear reversal indicators, do the possibilities of a profitable entry enhance.

IEMG, weekly chart. Supply: eToro

IEMG, weekly chart. Supply: eToro

Bitcoin: Fragile Equilibrium

Bitcoin enters the top of January in a part of fragile equilibrium, outlined extra by flows and positioning than by narrative. Worth stays steady within the USD 88,000–91,000 vary, however current actions make it clear that the market will not be being guided by a structural thesis, however by macro impulses and tactical capital reacting to headlines.

The most recent episode illustrated this properly. It was not a crypto catalyst that moved the market, however politics. The cooling of tariff rhetoric triggered a broad rebound in danger belongings. Bitcoin didn’t lead or decouple, but it surely adopted. The transfer was additionally amplified by leverage and resulted in a liquidation occasion, fairly than a clear entry of consumers.

This reinforces a well-known studying: bitcoin continues to behave like a danger asset, not a protected haven. When uncertainty eases, it holds up; when it intensifies, it fails to draw defensive flows, not like gold.

Beneath the floor, on-chain knowledge provides vital nuance. The market reveals cooling, not weak point. Community exercise has moderated, internet flows to exchanges stay detrimental, and a rising share of provide stays immobilized within the palms of long-term holders. Revenue-taking has fallen considerably in comparison with the fourth quarter of 2025. Put merely, much less is being offered and extra is being amassed, albeit with out urgency. Structural promoting stress is low, however that doesn’t indicate fast upside momentum.

In derivatives, using leverage has elevated once more, however in a contained method. Open curiosity has recovered after the cleanup of positions on the finish of 2025, with a predominance of lengthy positions and still-moderate funding prices. There aren’t any clear indicators of overheating, though an increase in funding above 5% would enhance the chance of draw back liquidations. The market has room to construct positions, however it isn’t “pressured” in any path.

The choices market reinforces this balanced studying. The “Max Ache” stage sits very near the spot value, which tends to compress short-term volatility. Skew is beginning to flip larger, with elevated curiosity in calls above USD 95,000–100,000, whereas places at decrease strikes proceed for use as institutional hedges. There isn’t a panic, however there’s warning.

As for individuals, the sample is obvious. Demand comes primarily from establishments, ETFs, and huge holders, with sustained accumulation flows. Retail traders are neither current nor anticipated. Sellers are primarily medium-term holders who proceed to take income progressively, with no indicators of capitulation. Miners and huge whales are lowering gross sales. The web steadiness favors structural consumers.

All of that is occurring at a time when the outdated map now not works. The four-year cycle now not explains market conduct by itself. Liquidity has concentrated in institutional automobiles that don’t rotate into the remainder of the ecosystem as they as soon as did, leading to a narrower, extra demanding, and slower market. In the meantime, infrastructure continues to advance (tokenization, stablecoins, 24/7 buying and selling), and utility is progressing quicker than value.

As issues stand, bitcoin will not be damaged, however it isn’t confirming a transparent path both. It’s neither in a breakout part nor in euphoria. Help is being constructed by quiet accumulation, not exuberance. So long as institutional flows proceed and leverage stays managed, the present vary is sensible.

The bullish catalyst stays the persistence of ETF inflows; the primary danger is an increase in leverage mixed with macro shocks. The market doesn’t want extra narrative. It wants indicators that may stand up to stress.

This communication is for info and schooling functions solely and shouldn’t be taken as funding recommendation, a private suggestion, or a suggestion of, or solicitation to purchase or promote, any monetary devices. This materials has been ready with out bearing in mind any specific recipient’s funding goals or monetary scenario and has not been ready in accordance with the authorized and regulatory necessities to advertise unbiased analysis. Any references to previous or future efficiency of a monetary instrument, index or a packaged funding product should not, and shouldn’t be taken as, a dependable indicator of future outcomes. eToro makes no illustration and assumes no legal responsibility as to the accuracy or completeness of the content material of this publication.

{kind=link}