Spotify’s inventory has been unstable through the years, however its enterprise has been pretty regular. The Every day Breakdown dives into the main points.

Earlier than we dive in, let’s be sure you’re set to obtain The Every day Breakdown every morning. To maintain getting our every day insights, all that you must do is log in to your eToro account.

Deep Dive

It’s that point of 12 months when Spotify offers us our year-end wrap — so we’re doing one for Spotify itself. As most readers know, Spotify supplies audio streaming companies worldwide via its Premium and Advert-Supported segments. The corporate, based in 2006 and headquartered in Luxembourg, has had a outstanding run as a public enterprise.

After greater than doubling from its 2018 opening value to its 2021 excessive, shares collapsed within the subsequent bear market, falling greater than 80% — 🫣. However the rebound was much more dramatic: the inventory rallied over 1,000% from these lows, finally reaching an all-time excessive of $785 in June 2025.

The Enterprise

Because the chart above reveals, premium customers, month-to-month lively customers, and income have continued to climb steadily through the years. Even throughout Spotify’s brutal 2021–22 inventory decline, the underlying enterprise saved increasing. Nonetheless, Spotify struggled with profitability for a lot of its historical past — from 2015 via 2023, it recorded just one 12 months of optimistic working revenue.

That modified in 2024, when working revenue surged, and it has grown even additional in 2025. This shift to sustained profitability is a significant cause the inventory has seen such a strong rebound from its lows.

Future Development Projections

After we look towards the longer term, analysts stay optimistic about Spotify’s underlying development potential. Discover how earnings development is way outpacing income development, which is an efficient signal for the corporate’s margins. In response to Bloomberg, analysts venture the next:

Earnings Development: 32.4% in 2025, 67.5% in 2026, and 27.7% in 2027

Income Development: 9.7% in 2025, 14.6% in 2026, and 13.9% in 2027

Analysts at present have a consensus value goal of ~$773.50 on Spotify inventory, implying greater than 37% upside to at this time’s inventory value.

Wish to obtain these insights straight to your inbox?

Enroll right here

Diving Deeper

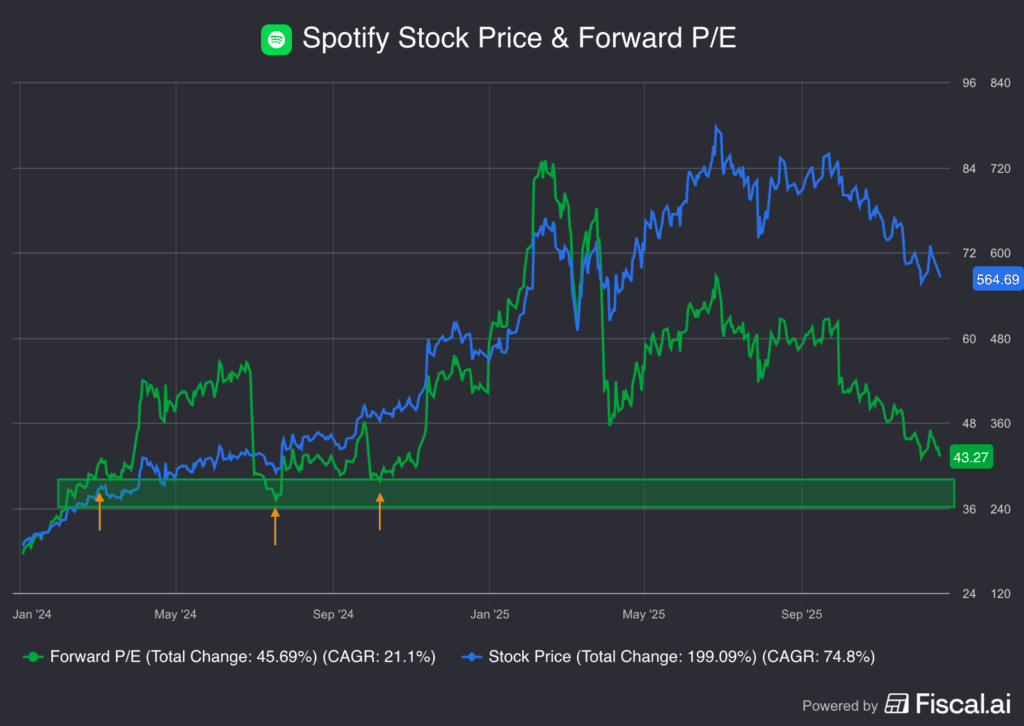

Now that shares have rallied greater than 1,000% from their current lows, Spotify’s valuation is beneath comprehensible pressure. Nonetheless, the inventory’s ~28% decline from its summer season highs has helped ease that stress. Earlier this 12 months, Spotify traded at greater than 80x ahead earnings, and even at its summer season peak — when shares hit file highs — the a number of was nonetheless almost 70x.

Now buying and selling round 43x ahead earnings, the inventory sits simply above the zone the place it has not too long ago discovered valuation help — roughly 40x. Whereas that is nonetheless costly by many traders’ requirements, the a number of has compressed considerably. Actually, valuation has fallen by nearly 50%, despite the fact that the inventory itself has corrected solely about half that quantity. That tells us profitability is shifting in the fitting course.

Dangers

Spotify competes in a troublesome panorama, going up towards giants like Apple, Amazon, and Alphabet’s YouTube. Aggressive stress is a continuing danger — and so is valuation. If development slows or expectations reset decrease, the inventory may face extra draw back. Buyers may additionally determine {that a} decrease a number of is warranted no matter aggressive efficiency. Lastly, Spotify has proven a bent to say no extra sharply than the broader market throughout pullbacks, that means any notable S&P 500 correction may hit SPOT disproportionately exhausting.

The Backside Line

Spotify has been a standout performer in recent times. For that to proceed, the corporate should uphold its robust development trajectory and hold boosting income. After the current dip, some traders will nonetheless view the inventory as too costly, whereas others might even see the valuation reset as a recent alternative.

Disclaimer:

Please notice that as a result of market volatility, among the costs could have already been reached and eventualities performed out.

{kind=link}