Fraud is rising extra subtle and has develop into supercharged by generative AI, deepfakes, and more and more organized social-engineering networks. The altering dynamics have pressured each banks and fintechs to rethink their defenses as criminals adapt sooner, extra incessantly, and with extra customized assaults. Throughout fintech, it’s clear that conventional fraud controls are now not sufficient to guard clients.

However whereas the whole business is going through the identical escalating threats, fintechs have been particularly artistic in rolling out new layers of safety. Over the previous 12 months, a handful of standout options have emerged that fight fraud by proactively shaping buyer conduct, interrupting social-engineering ways, and shutting gaps that legacy programs can’t attain. Listed here are three distinctive new improvements price watching (and borrowing).

Revolut’s geolocation restrictions

Revolut launched a security characteristic yesterday that permits customers to limit cash transfers to particular, user-approved geographic areas. If a switch request is made out of the shopper’s gadget, however takes place at a location that the shopper has not listed, the app blocks the transaction robotically, even when the fraudster has the consumer’s credentials. The characteristic makes use of each gadget GPS and Revolut’s inner danger engine to cut back account takeover losses.

Why banks ought to care:Geolocation locking provides a low-friction layer to fraud protection, particularly for decreasing licensed push cost fraud (APP) and account takeovers. By having the consumer decide their restricted, “protected” places, banks might supply customers extra granular management over how and the place their cash can transfer.

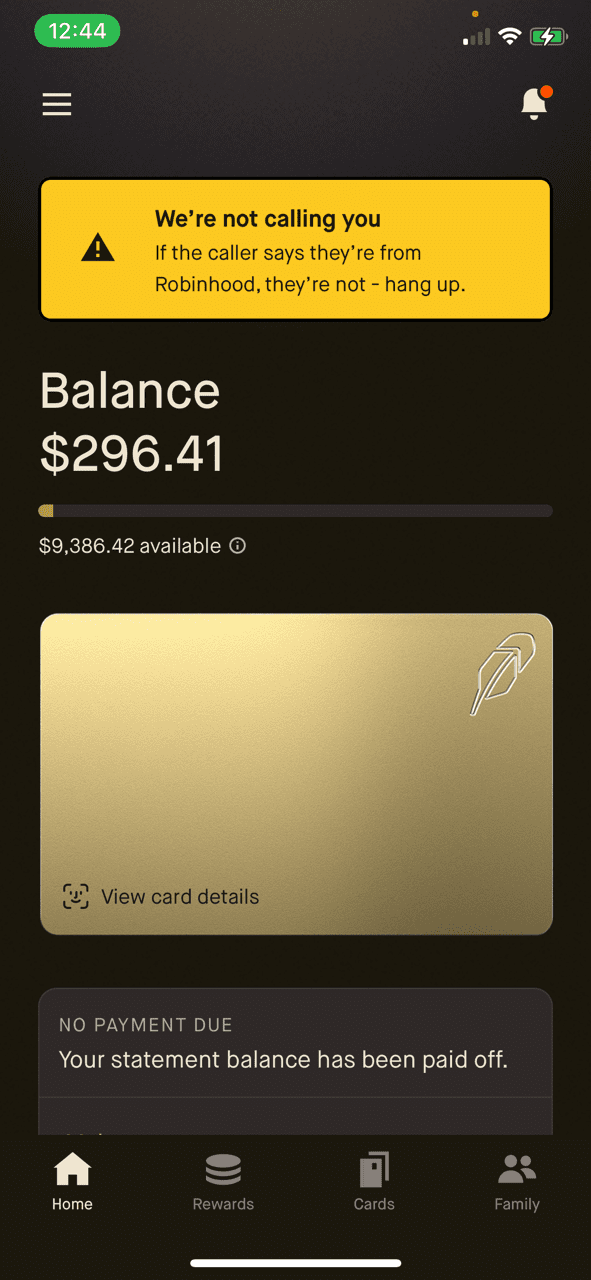

Monzo’s and Robinhood’s in-app rip-off warnings

Each Monzo and Robinhood assist customers decide whether or not an inbound name claiming to be from the financial institution is official. When a buyer is on a name and opens their cell app, the app shows a banner that clearly communicates that the decision they’re on is just not with the financial institution. In Robinhood’s case, the message states, “We’re not at the moment attempting to name you. If the caller says they’re from Robinhood, they don’t seem to be. Cling up.”

Why banks ought to care:Impersonation scams are one of the vital costly types of APP fraud. Including an in-app, real-time verification banner is an very simple however efficient approach to interrupt fraudsters.

iProov’s deepfake-resistant biometric verification

iProov is combating deepfakes with biometric verification that detects AI-generated faces and artificial video spoofing. The corporate analyzes pixel-level mild reflections, which it calls “liveness assurance,” and makes use of deepfake-detection fashions to determine whether or not a stay consumer is current. That is turning into important for distant KYC, account restoration, and high-risk authentication.

Why banks ought to care:Banks more and more depend on distant onboarding and passwordless authentication, however deepfakes at the moment are in a position to defeat most of the legacy selfie-verification programs launched prior to now decade. Deploying deepfake-resistant biometrics is turning into important to stop fraudulent account opening and social-engineering-driven account resets.

Every of those options has one factor in frequent: they put friction in precisely the fitting place. The friction isn’t utilized to each transaction, they usually received’t deter trustworthy clients, however they may assist cease fraud in frequent locations. By utilizing smarter triggers, real-time context, and design selections, fintechs are in a position to interrupt fraudsters. And whereas every resolution received’t cease all fraud, they handle among the heavy lifting whereas minimizing the burden of friction on finish shoppers.

Photograph by Pixabay

Views: 143

{kind=link}