Analyst Weekly, November 3, 2025

Commerce Diplomacy: US’s “Asia Blitz” Targets China

Whereas D.C. argued over spending, the US administration was busy redrawing Asia’s commerce map. Offers have been achieved with Malaysia, Cambodia, Vietnam, and Thailand, all carrying provisions designed to curb China’s affect, from banning items made with compelled labor to tightening export controls on delicate applied sciences.

On the identical time, Washington and Beijing reached a one-year “managed decoupling” truce: China paused new rare-earth export bans, the US delayed new sanctions on Chinese language corporations, and each side agreed to extra agricultural and power commerce. The purpose, a minimum of for now, is to gradual the financial separation with out derailing international provide chains.

Investor Takeaway: Count on renewed momentum in “China-plus-one” commerce beneficiaries like Vietnam, Thailand, and India. ETFs monitoring rising Asian manufacturing may achieve from redirected provide chains. US semiconductor and power exporters additionally stand to learn as commerce flows rebalance.

Allies within the Fold: Japan, South Korea, and the AI Angle

The US additionally deepened its alliances with Japan and South Korea, placing funding pacts throughout nuclear power, shipbuilding, and synthetic intelligence (AI). Japan dedicated to assist finance $80 billion price of US nuclear initiatives, whereas South Korea’s $350 billion funding plan, a long-debated bundle, will now prioritize heavy manufacturing and maritime industries.

In the meantime, tech cooperation took middle stage: Washington and Tokyo agreed to coordinate AI and quantum computing growth, making certain that allies depend on US-made AI chips. Taiwan additionally reported “progress” in its personal commerce talks, reinforcing America’s expertise sphere of affect.

Investor Takeaway: This “friendshoring” momentum is bullish for AI infrastructure and chipmakers tied to US provide chains. Names in semiconductors, clear power, and industrial robotics may see sustained demand. Lengthy-term buyers may take a look at international thematic funds targeted on AI or next-gen manufacturing.

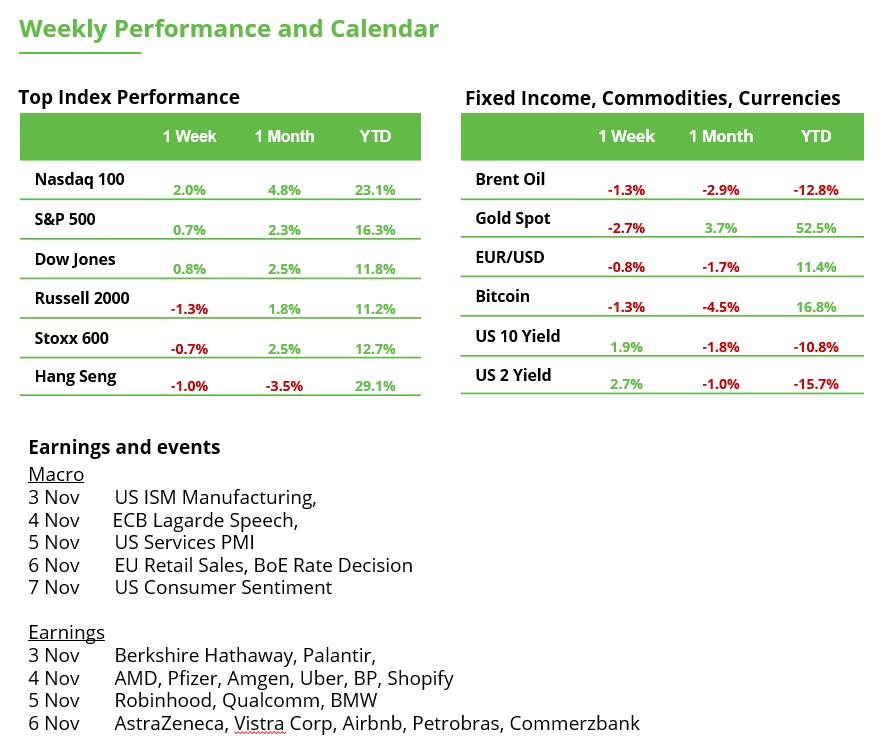

Key Earnings Stories: Week of November 3, 2025

Palantir Applied sciences (PLTR): Traders will probably be laser-focused on the uptake of Palantir’s new Synthetic Intelligence Platform (AIP) and its position in accelerating the corporate’s progress. The increasing industrial use-cases for Palantir’s AI-driven analytics have analysts predicting a ~50% YoY income bounce, underscoring the view that Palantir is on the forefront of the AI revolution.

Pfizer (PFE): Traders will probably be looking ahead to steerage and new product momentum, in search of indicators that Pfizer’s non-COVID portfolio (which grew 14% within the prior yr’s quarter) can offset the steep decline in COVID franchise gross sales and restore earnings progress.

Superior Micro Units (AMD): Wall Avenue is targeted on momentum in AMD’s increasing AI and cloud segments, anticipating ~27% YoY gross sales progress fueled by demand for EPYC server processors and new AI accelerators; a development buyers hope can hold AMD’s 2025 rally intact within the face of PC market headwinds.

Uber Applied sciences (UBER): The highlight is on execution and margin self-discipline as Uber strives for sustainable profitability throughout rides and supply. Traders are looking ahead to regular ride-hailing revenue margins and bettering unit economics in meals supply; stable bookings progress coupled with price management may lengthen Uber’s 2025 inventory surge, whereas any slip in effectivity or demand would increase doubts about its post-pandemic revenue trajectory.

BP (BP): The main focus will probably be on money movement and strategic portfolio strikes amid an unsure oil worth outlook. Traders are eager for updates on BP’s plan to promote its Castrol lubricants unit, a divestment aimed toward boosting shareholder worth, and can scrutinize how greater refining margins (anticipated to elevate quarterly earnings) are balancing out softer upstream earnings.

Qualcomm (QCOM): Qualcomm’s report will check whether or not rising progress areas can overcome weak spot in its core smartphone chip enterprise. Traders will gauge if demand for Qualcomm’s AI-enabled chips and growth into PCs, autos, and IoT can offset continued softness in international handset gross sales, the smartphone market stays Qualcomm’s stronghold however has been sluggish, so any commentary on handset demand or diversification (e.g. wins in premium telephones or PC processors) will seemingly drive the inventory’s response.

Shopify (SHOP): The e-commerce platform’s valuation rests on balancing speedy progress with bettering profitability. The important thing metric will probably be Shopify’s gross merchandise quantity (GMV) and income progress (guided within the high-20% vary) relative to its expense self-discipline, buyers need to see continued 20%+ GMV growth alongside proof that latest price cuts are boosting margins and free money movement, which might validate Shopify’s post-rally valuation.

McDonald’s (MCD): The fast-food big’s same-store gross sales combine is the crucial focus this quarter. Traders are watching how profitable McDonald’s new worth meal promotions have been in driving buyer site visitors versus their influence on common verify dimension; early analyst insights counsel the September launch of Additional Worth Meals seemingly lifted foot site visitors however dented common ticket, so the corporate’s comparable gross sales (anticipated ~+2.5% YoY) and administration’s commentary on pricing will set the post-earnings tone.

Novo Nordisk (NVO): The Danish pharma heavyweight’s outcomes will hinge on its blockbuster weight problems and diabetes medication. Ozempic and Wegovy now account for roughly 65% of Novo Nordisk’s gross sales, so buyers will probably be laser-focused on the quarterly income from these GLP-1 medicines. Any replace on demand vs. provide constraints for Wegovy, and Novo’s potential to maintain excessive progress within the face of latest opponents, will probably be pivotal in driving the inventory’s response.

Moderna (MRNA): Moderna’s narrative is shifting from COVID windfall to pipeline promise. With COVID-19 vaccine income sharply down, the important thing for buyers is any signal of stabilization in booster demand and progress in Moderna’s non-COVID pipeline. Specifically, updates on the uptake of its new fall COVID booster and the standing of upcoming vaccines (like RSV or flu) are essential – the market needs reassurance that Moderna’s subsequent technology of merchandise can fill the hole as COVID gross sales fade.

AstraZeneca (AZN): As a UK-based pharma big reporting this week, AstraZeneca’s core oncology and uncommon illness drug gross sales would be the focus. Traders are significantly tuned to progress developments for key most cancers therapies and the corporate’s outlook amid upcoming drug patent expirations. Any updates on its pipeline (particularly in areas like oncology and the burgeoning diabetes/weight problems market) and the way it navigates drug pricing pressures within the US and Europe will seemingly drive AstraZeneca’s shares following earnings.

Airbnb (ABNB): The house-sharing platform’s quarter will activate the energy of journey demand and reserving developments. The metric to look at is nights booked and common each day charges, as Airbnb has been posting round 8 to 10% income progress. Traders will probably be listening to administration’s commentary on reserving momentum into the vacations and any alerts of shopper journey urge for food or margin stress – this may decide if Airbnb can keep its post-pandemic progress trajectory and excessive profitability into 2026.

Amgen (AMGN): As a newly inducted Dow part, Amgen’s story is about new medication changing previous ones. The main focus is on whether or not Amgen’s lineup of newer therapies and its Horizon Pharma acquisition are producing sufficient progress to offset patent fades and biosimilar competitors on growing old blockbusters. Traders will parse Amgen’s earnings and steerage for proof that its modern medication (and price cuts) are driving income positive aspects, a key issue behind Amgen’s market-beating efficiency this yr, as this may decide if the inventory’s outperformance can proceed.

Market Pulse: Vol, Skew, and a GLD Hangover

Regardless of political noise, the S&P 500 traded sideways by way of the heaviest stretch of earnings. Volatility cooled as earnings rolled on, with the VIX slipping under mid-October highs. Massive Tech earnings have been combined: Meta and Microsoft slipped, whereas Google held up. A big gold name place that had pushed months of upside was lower, signaling that the metallic’s 2025 rally might have peaked.

Volatility stays inverted, with near-term possibility costs greater than long-term ones; a setup that normally normalizes as earnings move.

Investor Takeaway: With short-term volatility easing, broader fairness participation may resume, suppose mid-caps and worth shares. As gold cools, funds might rotate into equities or bonds. Traders in search of diversification may rebalance out of treasured metals and into dividend ETFs or high quality cyclical names.

Palantir: Sturdy Rally, Excessive Expectations Forward of Q3 Earnings

Palantir Applied sciences is ready to report its Q3 earnings after the shut on Monday. The corporate, which makes a speciality of knowledge analytics and software program platforms, now ranks among the many 20 most precious corporations within the S&P 500. The inventory has surged greater than 160% this yr.

The market is presently in a brand new upward impulse, with the long-term uptrend confirmed by a contemporary file excessive final week. Within the short-term the inventory seems barely overbought, because the RSI sits above 70. With a ahead P/E above 260, the basic valuation could be very excessive, rising the chance of a correction. Even minor disappointments may set off vital volatility.

Analysts count on Palantir’s income to have risen 50.5% year-over-year to $1.09 billion within the third quarter, whereas earnings per share are projected to have grown by 67.4% over the identical interval. Ought to the inventory come beneath stress within the coming days or perhaps weeks, there are two key assist zones (Truthful Worth Gaps) to look at:

$171.26 to $172.84 – a zone examined thrice already, with patrons defending it every time.

$160.87 to $161.06 – a deeper assist space that might come into focus if a correction unfolds.

Palantir, weekly chart. Supply: eToro

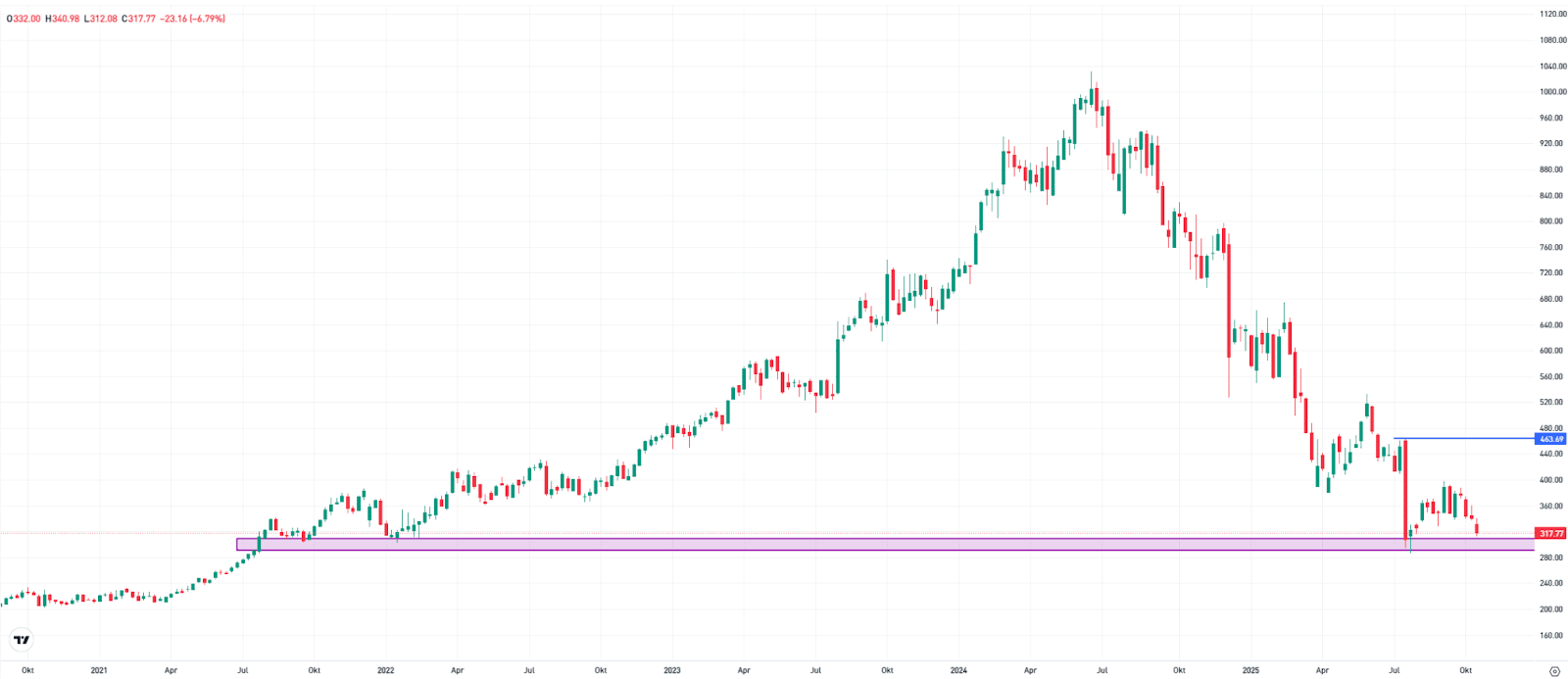

Novo Nordisk: Can Q3 Outcomes Stop Additional Losses?

Novo Nordisk will report its third-quarter outcomes on Wednesday earlier than the European market opens. The inventory has been in a downtrend for over a yr and has misplaced round 70% of its worth because the file excessive in July 2024.

In July and August, the share worth reacted to a long-term assist zone (Truthful Worth Hole) between 290 and 310 DKK, which dates again to the 2021 rally. Nonetheless, this response alone wasn’t sufficient to set off a sustained development reversal. Though there was a short-term rebound, solely a break above resistance at 463 DKK would considerably enhance the technical image.

The upcoming earnings report will seemingly be decisive, displaying whether or not Novo Nordisk will proceed its downward trajectory or if the long-term assist space presents an opportunity for a backside formation.

Analysts count on income within the third quarter to have risen 7.9% year-on-year to 76.9 billion DKK, whereas earnings per share are projected to fall 19.1% to 4.95 DKK.

Novo Nordisk, weekly chart. Supply: eToro

This communication is for data and training functions solely and shouldn’t be taken as funding recommendation, a private advice, or a proposal of, or solicitation to purchase or promote, any monetary devices. This materials has been ready with out bearing in mind any explicit recipient’s funding targets or monetary state of affairs and has not been ready in accordance with the authorized and regulatory necessities to advertise impartial analysis. Any references to previous or future efficiency of a monetary instrument, index or a packaged funding product should not, and shouldn’t be taken as, a dependable indicator of future outcomes. eToro makes no illustration and assumes no legal responsibility as to the accuracy or completeness of the content material of this publication.

{kind=link}