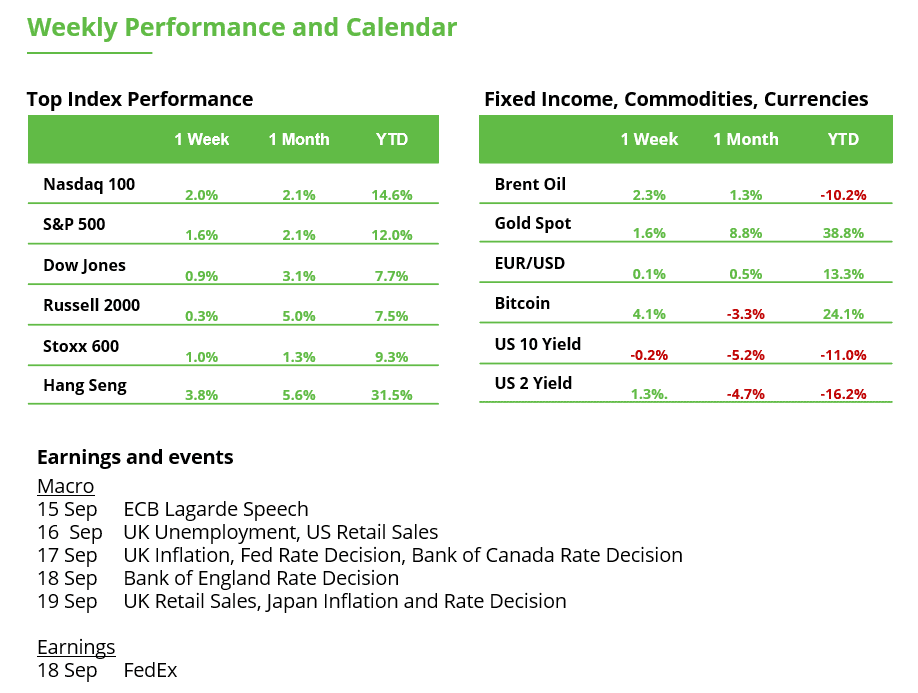

Analyst Weekly September 15, 2025

From EM tech energy to document US buybacks, market drivers are stacking up forward of the Fed’s first fee minimize of 2025. With US development nonetheless uneven and inflation expectations anchored, Powell is anticipated to ship a 25 bp minimize this week, however markets will likely be watching his steerage on the tempo of additional easing simply as carefully.

Tech is the New EM Engine

Rising markets (EM) have usually been seen as unstable and exhausting to navigate, however the newest earnings season suggests issues could also be turning a nook. Whereas general EM earnings development was flat in Q2, the breadth of earnings revisions is bettering for the primary time in months, particularly in Asia, because of tech energy and supportive coverage strikes.

Semis lead the pack: The standout theme is know-how. Corporations tied to the worldwide AI cycle are fueling earnings upgrades. Taiwan and South Korea, each tech-heavy markets, delivered stable revenue development because of robust demand for superior chips. Taiwan’s TSMC and Korea’s SK Hynix are clear beneficiaries, with management in areas like AI accelerators and high-bandwidth reminiscence.

Web shake-up: China’s huge e-commerce corporations like Alibaba, JD, and Meituan stay beneath strain from intense competitors, particularly in meals supply and fast commerce. Nonetheless, Alibaba’s cloud and worldwide companies are serving to offset home challenges. In the meantime, ASEAN web corporations corresponding to Seize and Sea are thriving. They’re displaying robust person development, resilient profitability, and increasing into fintech and digital companies. For buyers long-term structural development in EM, it is a key theme: the digital financial system is alive and effectively exterior of China.

Financials Regaining Power: One other brilliant spot is financials. Chinese language banks (like China Retailers Financial institution, Financial institution of China) noticed earnings rebound in Q2, helped by increased charge revenue. Indian and Brazilian banks additionally reported resilient outcomes, with names like ICICI Financial institution and Itau Unibanco highlighted as well-positioned leaders. Sturdy capitalization and regular mortgage development make them standouts in areas which might be nonetheless under-owned by world buyers. For retail purchasers, this implies the monetary sector, lengthy a spine of EM indices, is regaining relevance as a driver of regular returns.

Watch place sizes & FX Danger: EM strikes could be sharp, pacing publicity helps handle swings– broad EM or Asia ex-Japan ETFs assist clean out country-specific shocks. Pair EM tech/financials with publicity to gold (a basic EM hedge) or developed markets. To remove forex danger, buyers can put money into a forex hedged fairness ETF; exchange-traded forex (ETCs); or by way of CFDs or unfold bets.

Funding Takeaway: Rising markets might look boring on the floor, however momentum is quietly constructing. Tech is prospering, banks are stabilizing, and coverage help is boosting home demand. The scary “tariff shock” from US commerce coverage has been much less extreme than anticipated, giving exporters some respiration room. AI and tech cycles stay a worldwide resilience issue, serving to offset weak spots like shopper staples. Alternatives are broadening from Taiwan semis to Indian banks to Southeast Asian web platforms. With valuations nonetheless low cost and development selecting up together with Fed fee cuts, EM publicity could possibly be a strategy to steadiness portfolios tilted closely towards US mega-caps.

Large Buybacks, Larger Influence

US corporations are shopping for again inventory at document ranges in 2025. Almost $1 trillion in buyback bulletins have been made up to now this yr, placing 2025 on tempo to surpass final yr’s whole. Tech giants are main the way in which; Apple ($100B), Google ($70B), and Nvidia ($60B) all unveiled huge buyback packages this earnings season. Large banks like JPM ($50B), GS ($40B), WFC ($40B), and BAC ($40B) have additionally dedicated tens of billions every.

For buyers, buybacks matter as a result of they scale back the variety of shares in circulation. That may enhance earnings per share, present worth help, and sign that administration is assured within the firm’s future. However the exercise is extremely concentrated – a handful of mega-caps characterize about 66% of all buybacks this yr. For retail portfolios tilted towards tech and financials, that focus means buybacks may play an outsized position in driving returns.

VIX Slips as Markets Keep Pinned

Volatility retains grinding decrease (14.76), with the VIX sliding as key financial information passes with out sparking main swings. Market focus has shifted extra towards indicators of labor market weak spot than inflation, whereas the backdrop of attainable stagflation, slower development alongside sticky costs, stays a part of the dialog. AI-related shares past the “Magazine 7” have been a brilliant spot, serving to sentiment stabilize.

Nonetheless, supplier positioning into month-end suggests rallies are offered into and pullbacks are purchased, maintaining the S&P 500 range-bound. As soon as September choices and quarter-end expirations are behind us, the market may commerce extra freely, although company buyback blackouts might take away a layer of help. With volatility low, some buyers are eyeing October as a great window so as to add safety with methods corresponding to QQQ put unfold collars – which cap upside in alternate for cheaper draw back safety – drawing elevated consideration.

South Korean Shares With Dynamic Restoration

The EWY (iShares MSCI South Korea ETF) ended final week with a 7% achieve at 78.66 factors. In the long run, there’s nonetheless catching as much as do in comparison with the U.S. and European inventory markets. The final document excessive was reached on the finish of 2020 at 96.20 factors. The hole has now narrowed to 18%. Within the medium time period, buyers have more and more turned again to South Korean shares. Because the low in April, the index has risen 62%, whereas the S&P 500 gained solely 37% over the identical interval. From a technical perspective, EWY may proceed its restoration within the coming weeks and months – no less than so long as the help zone between 70.96 and 69.59 factors (Honest Worth Hole) holds.

EWY within the weekly chart. Supply: eToro

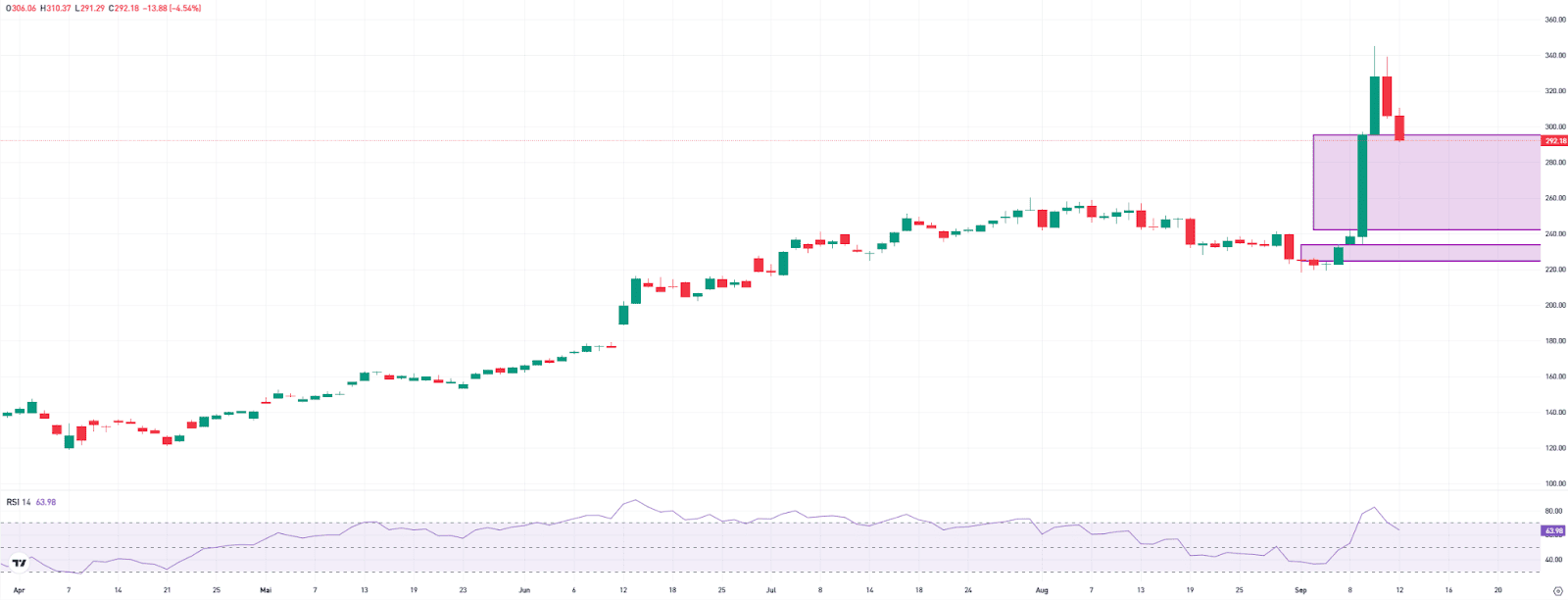

Cloud Enterprise Triggers a Surge in Oracle Shares

Oracle’s inventory skyrocketed final week, gaining over 25%. Sturdy cloud offers fueled a large order increase. In only one quarter, a number of multibillion-dollar contracts have been signed, together with with OpenAI, Nvidia, and TikTok. The order backlog surged to $455 billion — greater than 4 instances the earlier yr’s stage. On the danger aspect, Oracle faces extraordinarily excessive investments, which put strain on money circulate and margins. As well as, there’s a robust dependence on just a few main clients.

The market was closely overbought at instances, however situations have since eased considerably. Buyers ought to watch the reactions within the two Honest Worth Gaps created by the rally: between $241 and $296, and between $219 and $234. Bullish reversal alerts in these zones may point out {that a} new upward transfer is about to start.

Oracle within the each day chart. Supply: eToro

Macro Calendar: All Eyes on Powell

The Fed is anticipated to chop rates of interest on Wednesday for the primary time this yr (choice at 8:00 p.m.). Weak spot within the labor market provides the Fed the inexperienced gentle for a minimize. A small step of 25 foundation factors to a variety of 4.00 to 4.25 p.c is anticipated. By the top of 2026, markets count on a complete of six small cuts. Persistently excessive inflation may sluggish this tempo. That’s why the brand new quarterly projections from the central financial institution will likely be decisive. In June, the Fed projected core PCE inflation of two.4% for 2026 and a pair of.1% for 2027. A downward revision would give shares and bonds a lift. As well as, Jerome Powell’s press convention at 8:30 p.m. may present key steerage on what occurs after the September assembly.

This communication is for data and schooling functions solely and shouldn’t be taken as funding recommendation, a private advice, or a proposal of, or solicitation to purchase or promote, any monetary devices. This materials has been ready with out making an allowance for any explicit recipient’s funding targets or monetary state of affairs and has not been ready in accordance with the authorized and regulatory necessities to advertise unbiased analysis. Any references to previous or future efficiency of a monetary instrument, index or a packaged funding product are usually not, and shouldn’t be taken as, a dependable indicator of future outcomes. eToro makes no illustration and assumes no legal responsibility as to the accuracy or completeness of the content material of this publication.

{kind=link}