When bitcoin adoption reaches a world scale, it’s probably there’ll now not be bitcoin podcasts, bitcoin conferences and even, sorry to say this, a necessity for a Bitcoin Journal. Nonetheless, till this level, individuals curious about bitcoin can be differentiated from those that are but to start their journey down the bitcoin rabbit gap. The query is then raised, how does a bitcoiner describe themselves to others, that will assist bridge the chasm between their very own understanding and people nonetheless plugged into The Matrix?

Given the inflationary insurance policies of successive governments, globally (see Rune Østgård glorious e book Fraudcoin for extra info), practically everybody with assets has needed to develop into an “investor” merely to try to keep up buying energy extra time.

Individuals who need to personal the place they dwell, have the flexibility to personalise the place they spend their time, and (for essentially the most half) not be involved about eviction or be subjected to extreme prices of rental, mustn’t should view themselves as traders. Nonetheless, as a consequence of financial premia commanded by actual property, not solely do individuals have to take dangers by leveraging their property to buy houses (by mortgages), they might additionally want to invest that sooner or later, the worth of their residence can have elevated sufficiently to offset the prices incurred of buying, shifting and canopy the curiosity on their debt.

Alongside the necessity to construct wealth by “laborious property” comparable to property, the non-bitcoiner can be directed and infrequently supported in planning for the longer term by additional investments within the type of a pension. Whereas tax effectivity and, for these fortunate sufficient, extra employer contributions assist to extend advantages, the funding associated dangers are diminished. Nonetheless, these advantages additionally should be understood in relation to the counterparties concerned, comparable to adjustments in authorities coverage, adjustments in pension schemes or the worst-case situation of the corporate offering the pension experiencing monetary difficulties. Studying that the pension you have got been paying into for 30 years now has no worth by no fault of your individual is sort of merely heartbreaking to observe.

For the reason that public acknowledgement by Blackrock that bitcoin might not truly be an “index of cash laundering”, bitcoin as an funding grade asset is changing into an accepted narrative. This might imply that bitcoin can start to be thought-about alongside equities, actual property and pensions as a method on sustaining buying energy whereas additionally planning for the longer term. Nonetheless, trying again, this notion might merely be some extent on an ever altering journey, from its origins inside slightly recognized Cypherpunk mailing checklist that considered it as a collectible, by the medium of trade on the Silk Street to the place we’re in the present day. With an eye fixed on the longer term, it might be prudent to start considering of what description will come subsequent for somebody who owns bitcoin, that may make extra sense sooner or later aside from an “investor”. The very nature of bitcoin additionally means that it’s in contrast to different property (both commodities or securities), that means that it may be unsuitable to view it as both.

Sadly, according to consciousness of bitcoin not being even distributed, publicly held views of the asset are additionally slightly inconsistent. As just lately as Could, 2023, Harriet Baldwin MP, of the UK Parliament Treasury Committee really helpful that “unbacked ‘tokens’” (together with bitcoin), needs to be regulated as “playing slightly than as a monetary service”. Whereas that is largely true for “cryptoassets” extra broadly, that is merely unsuitable in relation to bitcoin, given it’s backed by the world’s largest pc community working a protocol that’s extraordinarily resilient to alter. The character of the bitcoin protocol implies that in contrast to actual property or pensions, adjustments in authorities, organisational insurance policies or an organisation’s efficiency can’t have an effect on its operation or utility sooner or later. Together with this, given the fastened provide of bitcoin, it’s also not subjected to debasement by inflationary insurance policies that impacts the unit of account for different property.

As a consequence, whereas previous information reveals the greenback worth of bitcoin is extremely risky (impacted by provide and demand dynamics), the dangers related to the asset itself are literally extraordinarily low. When that is mixed with the flexibility to self-custody the asset, at low value, additional dangers are eliminated when in comparison with the necessity for shares in firms or commodity certificates to be custodied by brokerage companies.

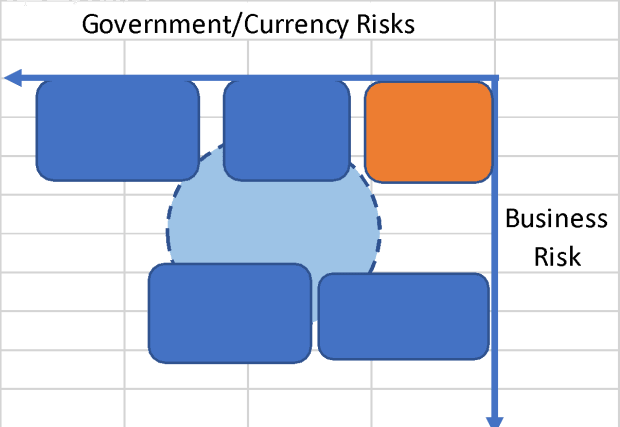

Normal definitions of investing focus upon an expectation that cash invested will develop, regardless that any knowledgeable investor will do that by balancing the potential development in opposition to any related dangers. From the treasury committee’s viewpoint, the dangers and returns related to playing would probably find bitcoin past the highest proper nook of the determine beneath.

From the angle of shopping for bitcoin being related in nature of playing, promoting a fiat forex for bitcoin, with an opportunity, slightly than an expectation of development might then counsel that bitcoin might not truly be capable to be classed as an funding.

To additional query the above determine, occasions seem to have modified from when this well-established concept was developed, precipitating the necessity for reflections on beforehand held assumptions. Authorities bonds are now not “threat free”, illustrated by the worldwide rates of interest will increase leading to dramatic losses within the worth of presidency bonds in 2022. This case has then impacted the dangers related to financial institution deposits, resulting in latest failures of enormous banks within the US. Compared to each authorities bonds and financial institution deposits, the safety of bitcoin is neither subjected to central financial institution rate of interest coverage threat nor third-party dangers related to the holders of presidency bonds (even when the short-term worth might change). Given the fastened emission schedule of bitcoin, it’s also not subjected to “cash printing” and authorities deficits which have diminished the buying energy of the underlying forex, as promoted by Fashionable Financial Principle.

Fascinatingly, in a latest doc from Blackrock, this contrarian viewpoint is supported, suggests a bitcoin allocation of 84.9% inside an funding portfolio, representing a really totally different threat profile when in comparison with different property (Thanks Joe). Except for the volatility related to markets making an attempt to cost a brand new asset, this implies that bitcoin is the place Blackrock would suggest holding the vast majority of your wealth. The determine beneath thus suggests another framing when evaluating bitcoin to different property, the place as an alternative of presenting returns on funding, consideration is given to the dangers of the underlying unit of account (fiat forex) in opposition to the enterprise threat.

Throughout the present excessive inflation surroundings, forex and enterprise associated dangers are heightened. Historical past then offers a sobering perspective on the impression of inflation on the well-being of a inhabitants (see When Cash Dies). Throughout Weimar Germany, because of the problems with the forex, those that invested skilled durations of constructive returns, however had been later ruined as hyperinflation took maintain. On this context, slightly than investing in gold, those that merely saved in it may trip out the risky worth actions. In an interesting echo, the identical has been demonstrated in Argentina in the present day with bitcoin. Buyers or merchants are more likely to have misplaced cash, however in the long run, saving in bitcoin has been a a lot better possibility for the common Argentinian.

So sure, I’m a bitcoiner, however that doesn’t imply I’m an investor, speculator, gambler or a felony and whereas I’d prefer to be, I’m additionally not a Cypherpunk. I’m merely somebody working in direction of a greater future for myself, my household and perhaps even their households. Bitcoin seems to offer a method of transferring the worth of my work in the present day into the longer term, with out the dangers of it being mismanaged (equities), legislated in opposition to (pensions), prone to central financial institution coverage (authorities bonds and fiat currencies) or struck by lightning (actual property). In consequence, bitcoin might not be an funding and is barely a hypothesis or gamble should you purchase it with out understanding it.

To return to the title, when requested about themselves and the way they’re planning for the longer term, a bitcoiner can merely say, “I’m staying humble, appreciating I’ve quite a bit to study however saving the perfect asset I can discover” (see Mickey’s work for a macro viewpoint). Hopefully, it will pique their curiosity, so result in the comply with up query of “are you able to inform me extra?”. At which level, the orange pilling can start.

It is a visitor publish by Rupert Matthews. Opinions expressed are totally their very own and don’t essentially mirror these of BTC Inc or Bitcoin Journal.

{kind=link}